- 11 views

“The patterns repeat, though the details never do.”

—Howard Marks, American investor and co-founder of Oaktree Capital Management

Silver, once the silver lining for the green energy and AI revolutions, is now becoming a strategic liability. Record-shattering silver prices—touching $116/oz in early January’26 before cooling to $80/oz—have raised tough questions about the Green Revolution's future, as soaring costs wreak havoc on the economics of solar and battery manufacturers.

While we can't predict the future, we can learn from patterns of the past. When a critical resource becomes a bottleneck due to price or scarcity, human ingenuity steps in to optimise its use or find alternatives.

In the 1960s, as global electrification accelerated, skyrocketing copper costs compelled power utilities to pivot to aluminium for high-voltage transmission—a shift that became permanent, thanks to aluminium’s lower density and abundant supply. Similarly, in 2011, when gold breached $1,900/oz, the semiconductor industry broke its centuries-old dependence on gold bonding wires, transitioning to copper for chip-to-package connections.

Today, the world faces a similar resource scarcity and high-price crunch with silver. The initial response from China's solar industry leaders is promising in tackling the shortage. If these alternatives deliver on their potential, we may witness the dawn of a new era in the electrical equipment industry: the "silver lining" giving way to "silver dotting"—where the metal is used only in microscopic amounts as a "seed," or removed entirely.

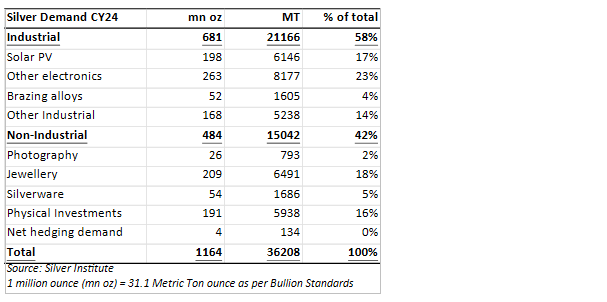

Understanding the industrial connection of silver

Silver is primarily an industrial metal, with 58% of CY24 demand coming from industry. Electronics and electricals led at 460.5 mn oz—the top driver—accounting for 68% of industrial demand (40% of total demand). Within this, solar modules consumed 198 mn oz (17% of total demand), semiconductors ~38.6–48.2 mn oz (Source: Shanghai Metals Market) and batteries an estimated 24–48 mn oz (our estimate).

Dissecting silver demand

3S, a key pillar for silver demand growth

The three themes of the modern economy—Solar, Energy Storage and Semiconductors (the AI Revolution)—rely on silver’s superior conductivity. These sectors are experiencing unprecedented growth.

|

Silver intensity of the Solar, Battery and Semiconductor

The $116/oz shock (even at $80, still a shock): A margin crisis |

Silver's ~175% rally over the past 12 months has jolted industrial users. While some face margin squeezes, others pass costs to customers. Solar suffers most: module silver costs doubled from 1.16 cents/Wp (at $40/oz) to 2.31 cents/Wp (at $80/oz), against a 9.6 cents/Wp ASP (China FOB – bifacial N-type module). Silver cost now accounts for 24.1% of the TopCon module price (at $80/oz), up from 12.1%.

Although batteries face a more modest impact (~0.75–1.5% rising to ~1.5–3% of lithium pack price), the higher silver intensity of solid-state batteries casts doubt on their commercial viability.

Solar industry at the forefront of de-silvering the manufacturing process

"I think frugality drives innovation, just like other constraints do. One of the only ways to get out of a tight box is to invent your way out."

—Jeff Bezos

Innovation drives solar and battery manufacturing, with ongoing improvements slashing costs and boosting efficiency. Heterojunction (HJT) cells—once the most silver-intensive—now lead de-silvering. Silver usage in HJT cells has fallen from 16 kg/MW in the beginning of CY24 to 6.39 kg/MW today, well below TopCon's 9 kg/MW.

To tackle the silver shock, manufacturers are deploying two strategies:

-

thrifting: using less silver

-

substitution: replacing silver

For PERC and dominant TopCon lines, thrifting involves swapping silver paste for silver-coated copper, with silver applied only at critical contacts. Upcoming HJT lines increasingly favour substitution through back-contact metallisation.

Chinese solar manufacturers are leading the charge against the silver rally:

-

LONGi Green Energy announced in January’26 that it will begin mass production of base-metal PV cells in Q2 2026, shifting to copper metallisation as rising silver costs strain supply chains.

-

As per Shanghai Metals Market, JinkoSolar has scaled silver-coated copper paste for TopCon, while Trina Solar is targeting pure copper paste in H1 CY26.

-

Aiko Solar commercialised a silver-free 10 GW back-contact line in January’26.

If the outcomes delivered by these industry leaders live up to their promise, the solar industry may soon press the fast-forward button on de-silvering.

In batteries, evolving solid-state technologies—the most silver-exposed—are also witnessing potential alternatives and progress. Research from Stanford University (January’26) shows that “doping” silver (applying an ultra-thin layer of silver and then heating it so that silver atoms diffuse into the host material), rather than “coating”, can reduce silver consumption.

Conclusion: Get pricey, get sidelined

The narrative of silver as an indispensable "green metal" is being rewritten. While silver’s conductivity remains unparalleled, the economic reality of $116/oz has turned it into a "luxury" component that global supply chains can no longer afford at scale.

The world now faces three choices:

-

pause the Green Revolution (an impossible choice), or

-

mine silver at a faster pace to reduce its cost (a possible choice), or

-

optimise its use and find cheaper alternatives (the most probable choice).

Sources: Bloomberg, PV Magazine, Infolink, Argus Media, UTI Research

The views expressed are author’s own views and not necessarily those of UTI Asset Management Company Limited.

All illustrations/ examples are purely meant for ease of understanding of the concepts and aid in planning by the investor. All illustrations/ examples that depict future values or other estimated numbers are based on reasonable assumptions and in no way give any guarantee or assurance or indication of the future performance. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this article, will be suitable for your portfolio. Please note that past performance may or may not be sustained in future and is not a guarantee of any future returns. The reader is urged to consult his or her financial advisor before making any investment decisions.

UTI Asset Management Company Limited (UTI AMC) or UTI Mutual Funds (UTI MF) along with its affiliates assumes no obligation to update or otherwise revise these estimates.

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

Deepesh Agarwal is working with UTI AMC Ltd as Senior Associate Vice President (Equity) – Department of Fund Management since November 2017. In research he covers Engineering, Infrastructure, Utilities and Textile sector. Overall, he has 10.5 years of work experience with last 4.5 years at UTI preceded by 4 years stint at Ambit Capital as Equity Research Analyst and 2 years at Hexaware Technologies as Corporate Finance Executive