- 4 views

Many investors are grappling with the uncertainty caused by the West Asia conflict. The objectives are unclear and the mixed messaging from the US administration is keeping Iran, as well as the global economy and markets, on tenterhooks.

In reality, markets are unpredictable and the unexpected does happen. However, it may not be unprecedented and that is the true value of studying history. If you don’t know history, everything appears unprecedented.

As an investor, the best way to be prepared is to learn from the history of the markets. That is the most reliable teacher of what one can expect during one’s own investment journey.

The fall in the Nifty so far is quite normal, as you can observe in the table below. The table lists the 10 largest drawdowns in the Nifty 50 over the past 20 years. The current fall makes it to the list but pales in comparison to the largest declines recorded.

A regional crisis that disrupts supply chains—especially oil—is not that unusual either. We saw the same in 2022 when the conflict between Russia and Ukraine broke out. That conflict still remains unresolved and continues at a lower intensity. How did the markets behave then?

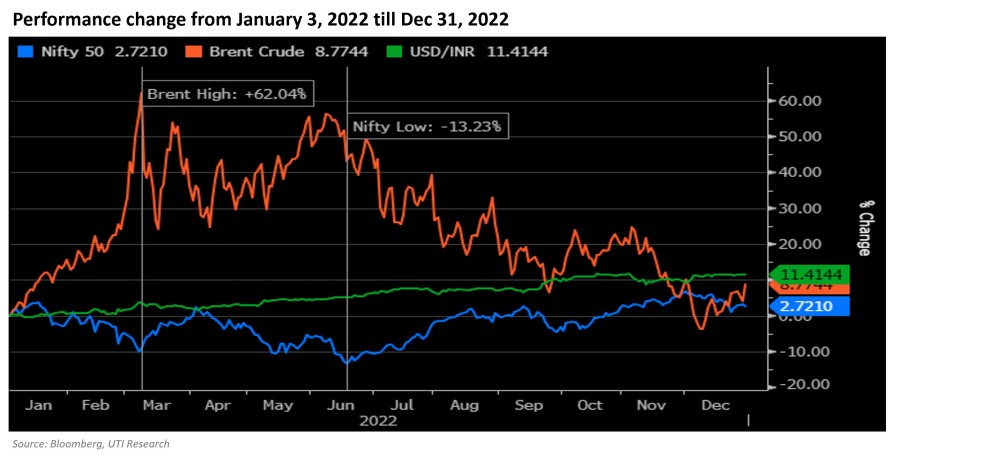

You can see the behaviour of the Nifty 50, Brent crude and the INR/USD exchange rate in the chart and table below. The chart tracks the percentage change in each of these three over the course of the year.

As you can see in the chart above, oil spikes nearly 62% higher for the year. At its worst point, the Nifty 50 is down 13% from the start of the year and the currency loses 12% at its weakest point from January 01, 2022. However, the patient investor experienced a different outcome by the end of the year. Oil is up merely ~9% for the year and the Nifty finishes higher for the year by ~2.7%.

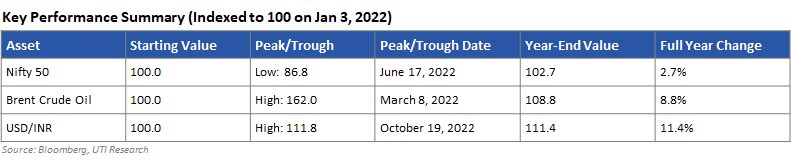

You can see the absolute values and the range during the year in the table below.

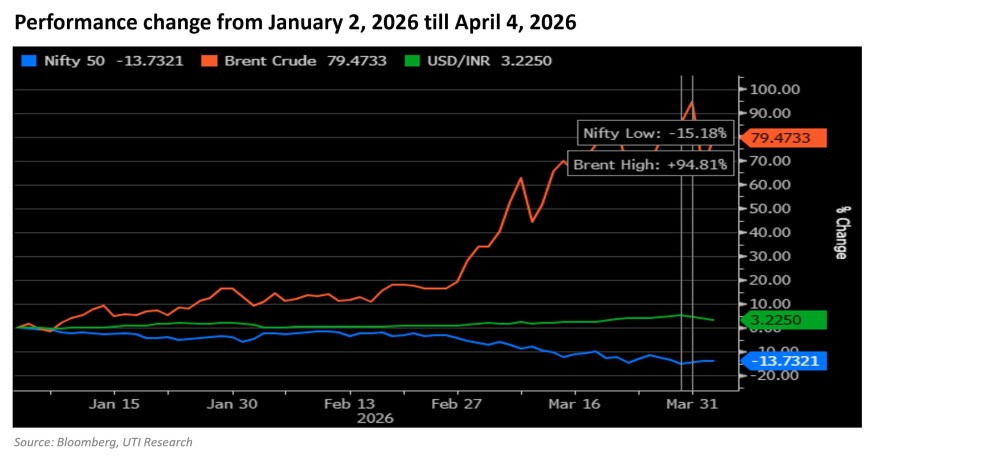

In the context of the above behaviour, the moves so far do look similar, as you can see in the chart below.

We do not yet know how this situation will evolve or reach a resolution of sorts. The world is unlikely to revert to the exact situation that prevailed prior to the geopolitical crisis. But our underlying assumption is that it is in everybody’s interest for some degree of normalcy to return, albeit with new frictions and additional costs that the global economy will have to bear.

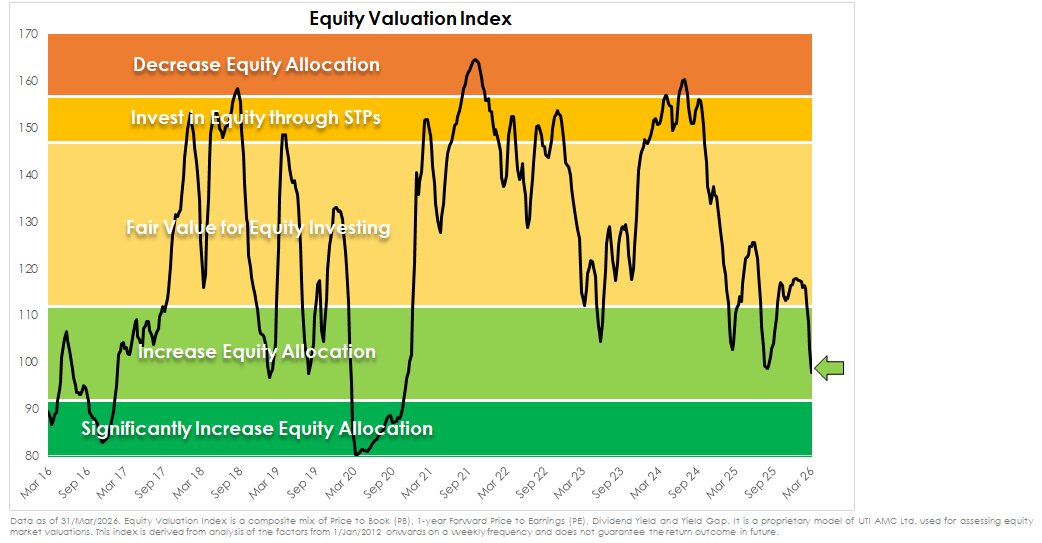

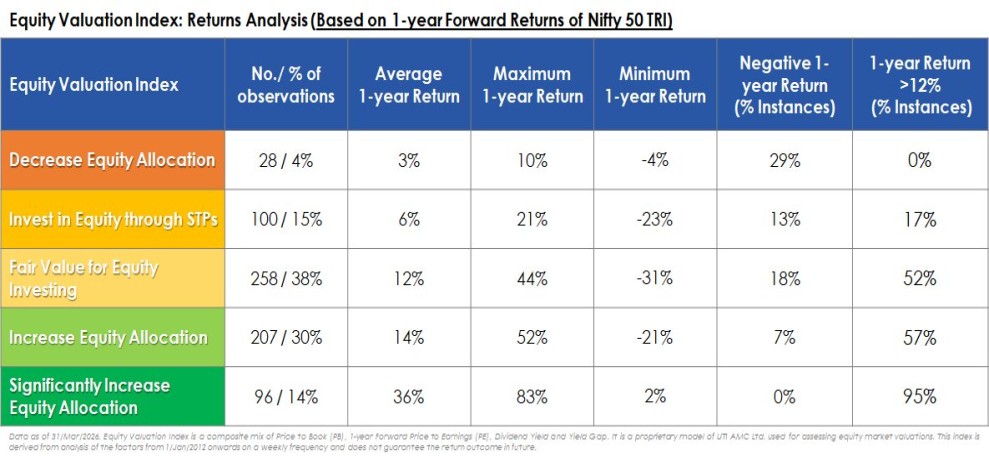

As investors, it pays to respond to events based on a plan rather than to speculate about likely future paths. Any plan that rests on asset allocation would now look favourably upon equities, given that current valuations appear attractive relative to history. Our Equity Valuation Indicator in the table below is now in the ‘green zone’. This indicator is a composite that incorporates Price to Book, 1-year Forward Price to Earnings, Dividend Yield and Yield Gap.

At this level, the indicator points to a degree of margin of safety that is now available to equity investors. The indicator is modelled on the Nifty 50, and therefore, the guidance from the model is applicable to large caps.

As for mid-caps and small-cap stocks, our fund managers see bottom-up opportunities in this segment of the market. However, given their aggregate valuations, we don’t see the margin of safety that would make us comfortable to make a top-down allocation call.

The table below highlights the risk-reward of investing in the markets (with the Nifty 50 as a proxy) during the differently coloured periods, which reflect the composite equity valuation indicator.

In the green zone -which is where the market is current positioned the history of returns points to a 57% probability of a return >12% over the next year. Historically in this range the probability of a negative return over 1-year is 7%. The average return over the next 1-year is 14%. The range of returns varies from +52% to -21%.

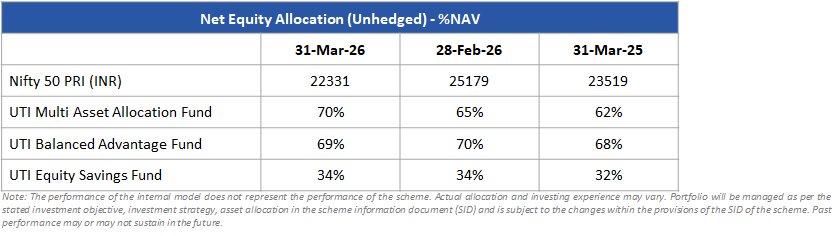

In line with the improved risk-reward scenario the hybrid funds at UTI Mutual Fund that rely on this model have raised their allocation to equities, as can be seen in the table below.

The key point which has changed compared to market peak in September 2024 is that the risk-reward is now attractive and investors with a long-term plan must take advantage of the opportunity. “Crossing the river by feeling the stones” is a famous Chinese idiom that feels quite apt in the current situation. It reflects an incremental and pragmatic approach to navigating unknown and complex situations. It is time to enter the water.

Vetri Subramaniam is the MD & CEO Designate at UTI Asset Management Company Limited. He holds a B.Com degree from University of Madras and a Post Graduate Diploma in Management from Indian Institute of Management, Bangalore. He joined UTI AMC as Head of Equity in January 2017, was elevated to Chief Investment Officer in August 2021 and has taken on the role of MD & CEO Designate. Prior to UTI, he held leadership and investment roles at Invesco Asset Management Private Limited, Motilal Oswal Securities Limited, Kotak Mahindra Asset Management Company Limited, SSKI Investor Service Private Limited and Kotak Mahindra Finance Limited.