Value Investing is dead was the oft repeated conclusion of investors who were being fed by commentaries of the investing community in early 2020. The conclusion was backed by not only short term performance data of 1 to 3 years performance but even looking at performance data of longer period of 10 years of value as style as compared to growth. It was difficult to imagine, during the period when the pandemic and its various waves were ravaging much of the developed and developing world, that value investing would start outperforming growth. Whether this is just a short term deviation from long term trends or a change in long term trend is unknown at the moment. What is known is that, those who changed style from value to growth when the noise against value was deafening got worst of both the worlds. This was also a practical lesson which we in UTI have being religiously following i.e. follow and stick to a well-articulated investment style consistently rather than drift over the styles based on the changing seasons. Therefore, UTI Value Opportunity Fund continues to be managed with its investment style of following intrinsic value approach rather than move to multiple driven approach just because the season has changed.

Our core belief remains that market has moved away from the approach of “cigar butt investing” (Inspired from the blog written by Howard Marks in Jan 2021) which essentially meant buying a company at significant discount to liquidation or replacement value or book value. The kind of free lunches available in the age of information asymmetry are hardly available now, and in case something is really cheap as compared to its liquidation value or for sake of convenience its book value, generally that company is dealing with specific issues. These kind of free lunches are now available only during times of significant market dislocations. The approach of buying a bond at 80% of maturity value hoping for full repayment at maturity including coupons work well in debt investing but caps upside in equity investing. Applying such approach to value investing essentially means investor is only buying stock at say 60-70% of book value for the stock and expecting that to move to 100% of book value, essentially selling off post it reaches 100% as no more “value” is left in that trade. This is a very narrow interpretation of value and in many cases have left to significant erosion of principal as investors fail to account of capital requirement of such businesses or inability to monetise the resources which were part of their net assets.

In the case of banks many were available at significant discount to book value over 2015-2019 period, following reversion of mean or discount to book value strategy turned out to be a very expensive way to learn the lessons. Many of these banks had significant capital calls arising out of assets which had turned bad and needed to mark down close to zero. This required huge dilution for the banks at prices which were at discount to book value. Hence a stock which was apparently available at 0.5x P/BV was no longer cheap when it had to dilute 50% at that valuation as book value eroded significantly. In many cases such dilution even happened multiple times at such cheap valuation leading to 2-4x dilution and 50-75% BV erosion. In these case theory of cigar butt investing turned out to be costly.

During the real estate sector boom in 2006-08 many companies got listed and the dominant investment argument was the inherent value of the land bank and company’s ability to convert that land into cash flows for investors. Most arguments for investing in the sector were driven by the belief that once these land banks will be developed the cash flows discounted back to present day were at significant premium to current prices. The fact was the sector was unregulated and the ability of converting those land bank to assets which could be sold was untested. When these factors played out the entire investment arguments proved unrealistic.

Unit economics driven dominant companies

The last few years have seen significant outperformance of companies which on the surface are reporting losses, but market is looking through it and valuing them based on ability to scale up at very little incremental capital. Telecom is one sector which has seem a dominant player emerging as number 1 player after investing massive amount of capital although incurring losses for few years.

Many new sectors driven by digital economies are difficult to imagine/ value from a traditional approach to investing which is driven by cash flows discounting while these sectors are largely driven by cash burn in the initial few years. The investing approach to such a business should be driven by understanding addressable market, the unit economics, how quickly or when that turn positive and start reflecting in the cash flows of the company. Also the ability of the company to scale-up with positive unit economics determine the growth runway for the company and its true value.

Option values

Many companies invest in adjacencies or as part of core business expansion in related ventures, most of these ventures or investment fail or are value dilutive. Investors dislike companies investing in non-core areas. However, in some cases such investments may create a valuable franchise which are option values for investee companies.

In some cases, the value of these investment exceed the value of the underlying businesses. Headline valuation don’t capture such options being created which have immense wealth creation potential. Many of these investments are in the form of lending brand names to subsidiaries which do not entail actual cash investment but help create significant value for the invested companies which also reflect in the valuation of investee companies stake in invested companies. In addition to actual capital invested, what is increasingly important is the value of brand which can be used by creating adjacencies, human capital which can be attracted, retained and deployed in new ventures and ability to innovate by using technology.

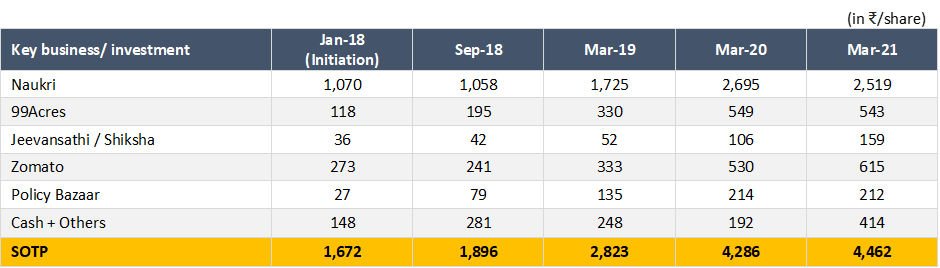

Info Edge is a good example of a company investing in many verticals as part of its core business while also making investment in business managed by competent individuals who needed capital. Value accretion has been exponential in these businesses over last 4 years. From an investment point of view, from valuation front it was expensive in 2018 but the kind of option values it had in the form of investment left enough opportunity for an investor to participate in value unlocking of these investments. That’s also value investing for us.

Sum-of-the-parts (SOTP) valuation of key businesses and investments of Info Edge (India) Ltd.

Source: Ambit Capital (Estimate)

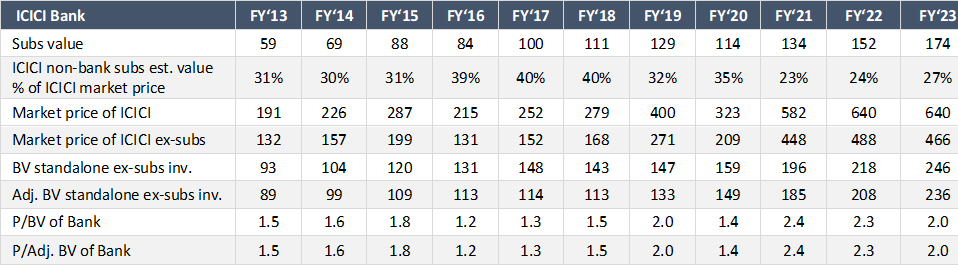

Banks which are regulated and have restriction in terms of capital invested outside the banks have made value accretive investments in adjacent businesses. An investor in ICICI Bank /SBI was not only investing in the core bank in early 2010s rather it was an investment in a holding company which have many subsidiaries with potential for value unlocking.

These investments have created a large cushion in the balance sheet of these banks and helped them provide for losses arising on account of corporate credit turning bad in 2015-18. Value unlocking through subsidiaries listing or sale down of stake helped them raise capital during tough times. ICICI Bank has seen almost 3x increase in value of its stake over last 7-8 years and this is despite its stake in these subsidiaries going down sharply post listing and divestments, so actual increase in value of these subsidiaries has been much sharper. Value investing includes identifying these option value which are part of the company specially when markets are focused on immediate problems facing the company.

Source: Kotak Institutional Equities, UTI (Estimate)

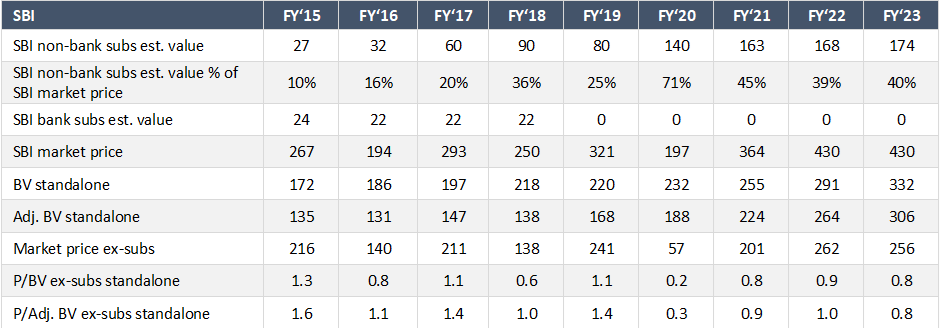

Pure multiple driven strategy would rarely envisage a situation that a PSU bank which was trading at 1.3x book in FY15 at the start of the Asset Quality Review (AQR) cycle will manage to come out of the cycle without raising too much dilutive capital on the back of sharp value accretion from subsidiaries and consequent listing. SBI’s non-bank subsidiary share of the market cap has moved from ~10% to more than ~40% in last 6 years as per our estimates. Hence it’s a value play not only on account of its cheap multiple but also due to its ability to create substantial value through its subsidiaries which went ignored during tough times.

Source: Kotak Institutional Equities, UTI (Estimate)

To conclude, we are unaware about any specific holy grail of investing. What is important for us is to stick to our investment style consistently and not drift away from the style based on flavour of the season. Our philosophy of approaching value through the prism of intrinsic value gives us flexibility to invest in companies with inherent option values in the businesses which widen the scope of investible stocks as well as would reduce portfolio volatility and return divergence. We endeavour to maintain discipline by building guard rails for our investing style and also realign, if needed.

| To read, Part-1 of What is Value? Click here |

Disclaimer: The views and opinions expressed in this article are those of the author and do not necessarily reflect the opinions or views of the organization.