- 1 view

As the fund manager of UTI Value Opportunities Fund, I often wonder if it would be more palatable to many investors if we called the fund ‘UTI Opportunities Fund’ (as it was once called) because the word ‘Value’ in the name of the fund has become unappealing to some.

This is rather strange given that we are a country in which ‘value for money’ is the mantra for both consumers and businesses. I was taught very early that ‘Price’ is what you pay, ‘Value’ is what you get. In the similar context, as I manage the mandate of the Fund, the focus is on for buying businesses for less than its ‘Intrinsic value’.

Intrinsic value was best described by Warren Buffet as - Intrinsic value is an all-important concept that offers the only logical approach to evaluating the relative attractiveness of investments and businesses. In simple words, Intrinsic value is “the discounted value of the cash that can be taken out of a business during its remaining life”. Of course an important caveat to this was provided by his long-time business partner Charlie Munger. In his words - Warren often talks about these discounted cash flows, but I’ve never seen him do one.

In common market parlance the term ‘Value’ has come to denote cheap valuations typically a low price to earnings (P/E) or price to book (P/B) rather than the concept of ‘Intrinsic value’. For us, ‘Value’ is a reference to ‘Intrinsic value’ and there are many ways to derive intrinsic value, one which is most elegant among them is a ‘discounted value of cash flow’, but it also a most trickier one because of the assumptions which goes into deriving a single number. Those assumptions are the risks – both to the upside and downside.

The central concern therefore I believe is not the term ‘Value’ but in what it has come to mean i.e., investing in stocks which are trading at cheap multiples such as low P/B, low P/E or high dividend yields.

A reason why this cheap multiple driven approach to ‘Value’ is not working is that, in fact, cheap valuation could be misleading. It does not take into account issues such as capital allocations, low terminal value, poor cash conversion/ free cash flow generation, recurring one–off negative surprises, agency problems such as unrelated/ uneconomical diversifications, incentive misalignment, corporate governance, treatment of minority shareholders etc. There is a very high chance for any or some among this varied list of reasons to show-up often in cheap valuations. A reliance on only statistically cheap valuations that ignores these factors, perhaps result in poor investment outcomes. Let’s explore them in detail.

Capital Allocation

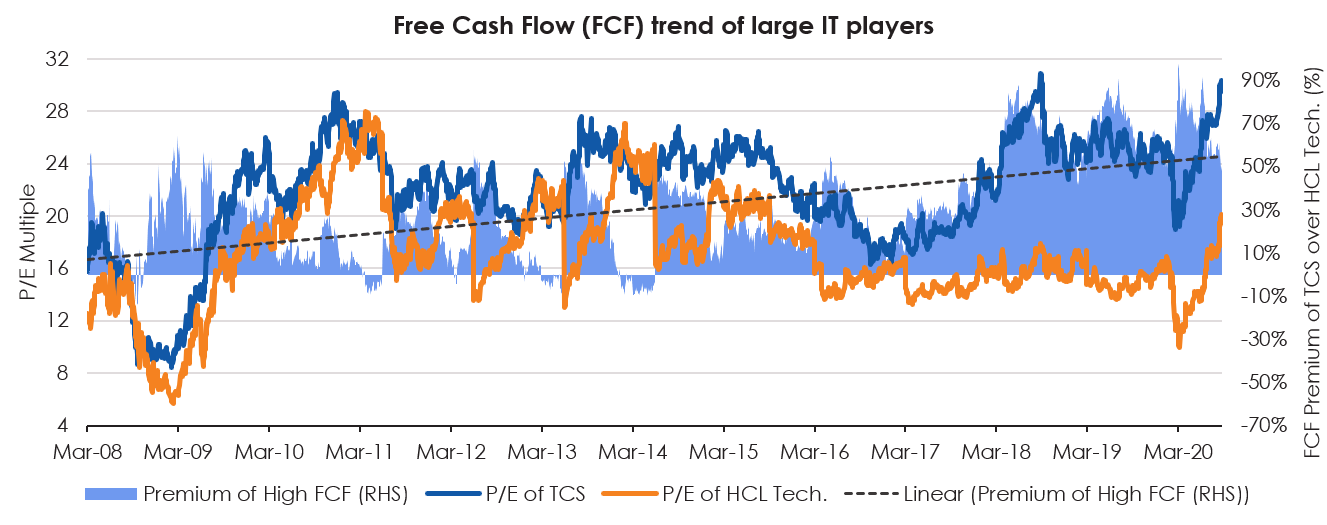

Rapid economic growth brings with its management obsession of growth at any cost, some of these costs are in the form of buying assets with leverage or at prices which generate return on invested capital (RoIC) which is sub-optimal with myopic promises of synergy. Some of the companies operating in sectors which generate strong cash flows have also embarked on the path of growth through acquisition. For example, IT as a sector has seen few companies buying growth through merger & acquisition (M&A) which consumes significant part of the cash flows. On the other hand, many others have chosen organic growth and returned cash generated to shareholders. In most cases, the first set of companies have seen multiples getting adjusted for buying expensive while those who rewarded shareholders through buy backs/ dividend have seen multiple expanding.

Source: Bloomberg. Data as of Sep-2020

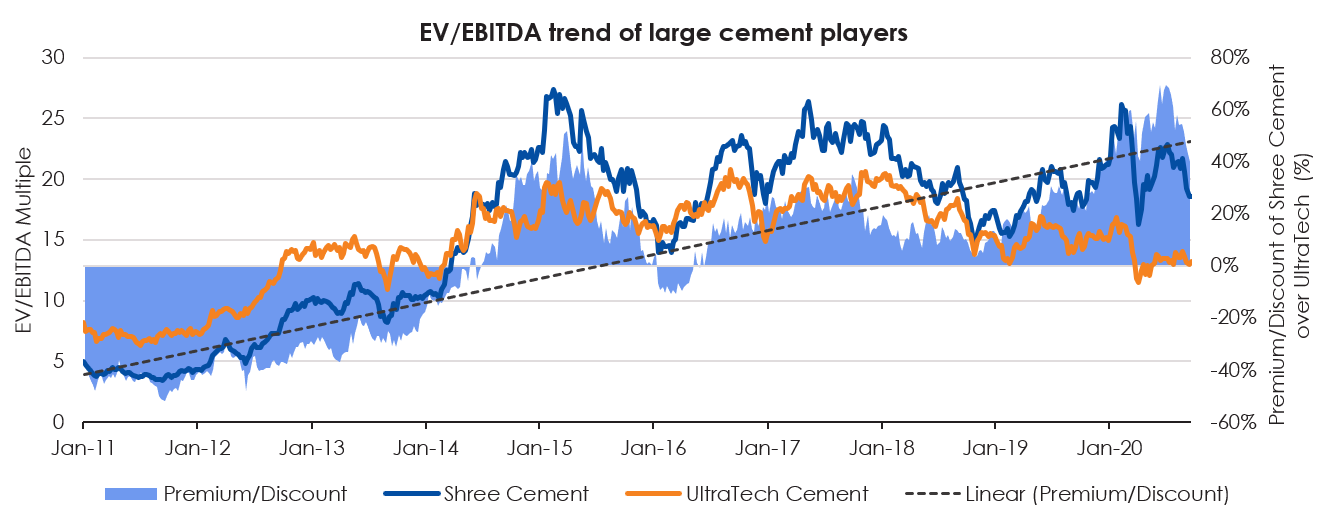

Similar issues have led to divergent valuation multiples within cement sector where managements have choices between acquiring cement plants or organic expansion through capex on clinkers/ grinding units. Growth through acquisition is generally at much higher costs than building assets leading to divergent return on capital employed (RoCE) outcomes. Management choice is between acquiring an operational capacity or investing in Greenfield/ brownfield expansion which will take time but will be cheaper. Efficient companies who manage to grow organically at reasonable costs end up with much better RoCE profile. While companies who are otherwise efficient but grow inorganically end up having much lower RoCE outcomes as they acquire based on competitive bidding. Market multiple end up capturing/ reflecting this divergent strategy.

Source: Bloomberg. Data as of Sep-2020. EV – Enterprise Value, EBITDA – Earnings before interest, taxes, depreciation & amortisation

Arranged M&A

Over the last few years, we have witnessed the Government exiting from a few public sector undertakings (PSUs) by selling stakes in one PSU to another PSU. The buyer may not be the originator of the transaction. Valuation could be cheap, however the cash utilised could have been used to pay dividend or reduce debt or deploy it in other productive opportunities. This situation has turned quite interesting in the financial space with public sector banks (PSBs) getting merged based on objective of creating few large PSBs which remain relevant in the fast-changing digital landscape. Some PSBs which should have focussed on growth post dealing with corporate credit risk led crisis, are now dealing with merger pains. In another such case, one large non-banking finance company (NBFC) bought the Government stake in another large NBFC by borrowing money, no share swap was done.

Source: Bloomberg. Data as of Sep-2020

Low Terminal Value

Over the last few years, we have seen global discourse on natural resources changing with focus shifting to environmental sustainability and impact on climate change through unbridled use of such polluting resources. Many companies operating in these sector are highly profitable, available at single digit earning multiple or double digit dividend yields. Yet anyone investing in them say 10 years back, looking at valuation would be disappointed today as they have only become cheaper. What we missed in the last decade was the rapid deterioration of the terminal value of such resources companies. When investors value a company at present value of the cash flows, large part of it come from future years which for the sake of simplicity is converted to terminal value, which is now at risk. Ability to extract the resources and actually use them have become questionable given our climate change commitments.

Worry over terminal value is also now reflected in the auto and its ancillary space with fear of electric vehicles (EVs) reducing terminal value of internal combustion (IC) engine driven business models. Even sector like visual media is facing value erosion through multiple compression on account of expansion of over the top (OTT) platforms, despite almost double-digit free cash flows yield of some of these companies.

Source: Bloomberg. Data as of Sep-2020

Management Continuity

Investors abhor uncertainty. Management stability is one way to give confidence to investors on corporate outlook and strategy. Frequent management churn creates instability in strategy while guidance on outlook is less credible. Across sectors, companies with stability in senior management and relatively long tenures have outperformed companies which have seen frequent changes in senior management. Private banking was one sector which had seen relative stability in management tenures, however over the last 3 years, we have seen significant changes in senior management on account of age cap or regulatory intervention. Multiples have invariably corrected on a relative basis as timeline of changes approach.

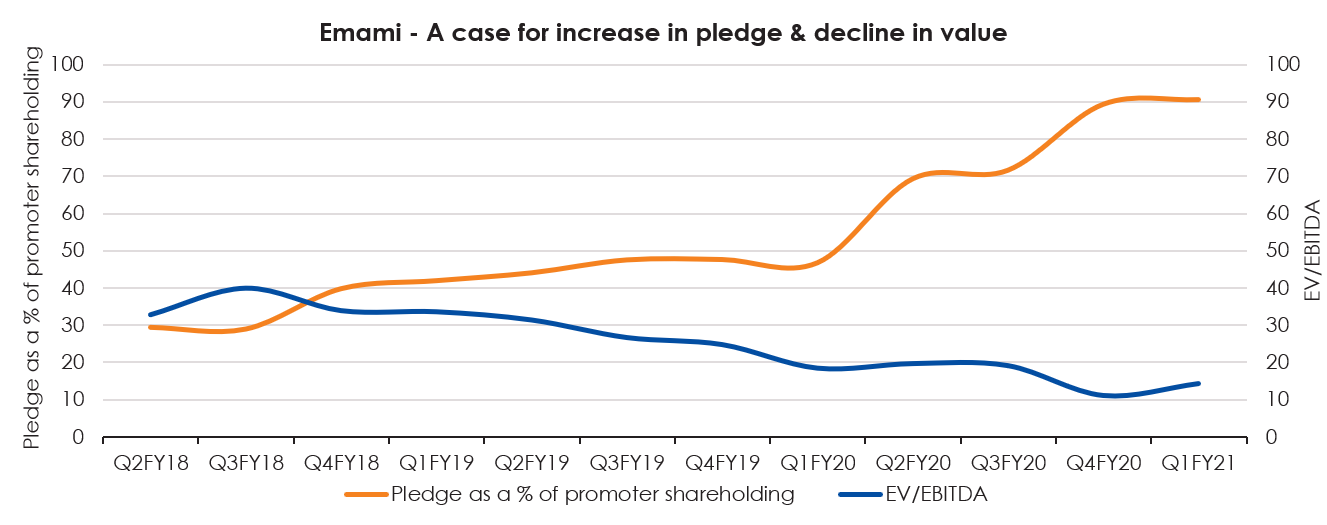

The Promoter Pledge

The agency problem arises when Promoter (i.e. management interest) is not aligned with minority shareholders. One version of this is when promoters pledge a large part of their stake in listed companies to invest in new ventures which are privately owned. Effective promoter ownership in such cases drops, as the stake has been effectively monetised in the form of debt. In many such cases promoter’s intention is to finally pay down the debt and remove the pledge. However, in a few cases things don’t work out as planned and the reflexivity of the market takes over and soon value of promoter stake is so low that they could lose interest. Further, there is a potential conflict of interest between the public company and the private venture. The valuation of the business goes down till the issues are resolved or company find a white knight. The subdued valuation multiple may have no underlying connection with the business outcomes but is a reflection of promoter pledge.

Source: Bloomberg. Data as of Jun-2020

Misalignment of Interests

Misalignment of shareholders’ interest and management interest is also visible when companies are asked to perform social obligations. It’s not that profit and social objectives are always in conflict, but we have seen companies being increasingly used to meet social outcomes of policymakers which by itself have tremendous value for the society. Unfortunately, in many cases the costs are borne by a set of companies. For example, select set of banks have disproportionately large part of the Jan Dhan account share which have sharply increased financial inclusion (Government objective) while cost of operating those accounts are largely borne by banks (~1.5% cost of operation of a savings account). Recently utilities have been forgoing fixed or capacity charges levied on state electricity boards (SEBs) facing financial difficulties in COVID-19 led slowdown, this was applicable to all utilities.

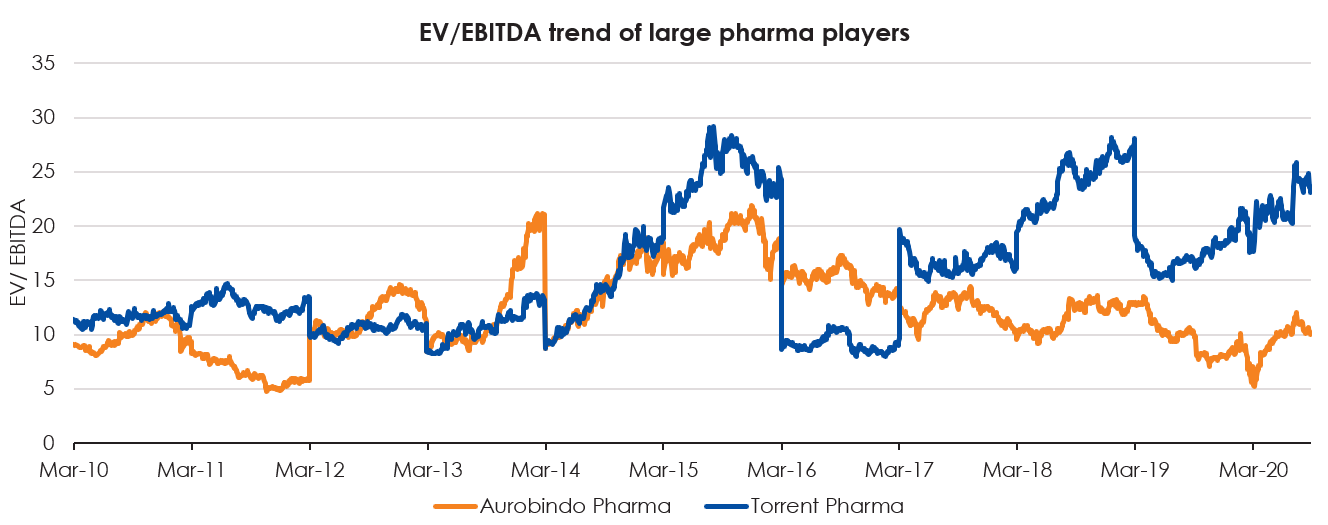

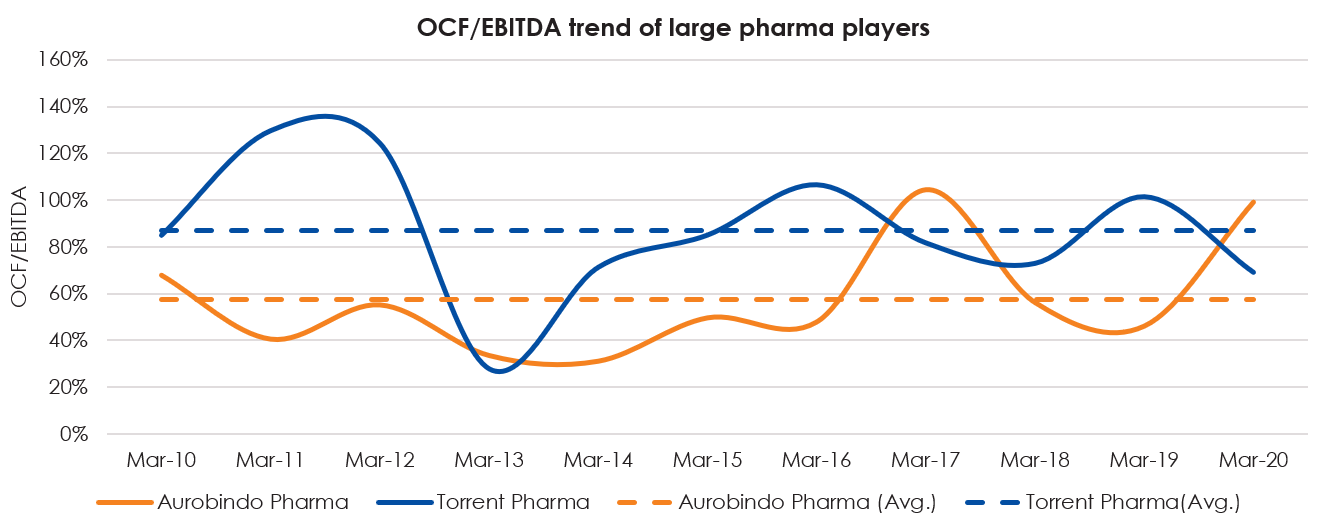

EBITDA to OCF Conversion

Working capital intensity of businesses are different, in some sectors customers pay in advance while suppliers are paid with a lag and inventory is fast moving. This results in negative working capital in many cases which leads to low capital intensity of the business. While in many other businesses revenues are booked upfront and actual cash flows changes hand with a lag leading to working capital expanding and making it a capital intensive business. In both the cases EBITDA margins may be same, but conversion of EBITDA to operating cash flows will be determined by what is cash conversion cycle of the business. Low working capital intensity will lead to higher % of EBITDA converting to operating cash flows while higher working capital will have opposite effect.

Headline valuation of business models with high working capital will appear cheap but that’s just market discounting the respective cash flow profiles. Even in sectors with strong cash flows profiles like pharma, companies have divergent cash conversion cycles on account of different timeline of conversion of revenue to cash.

Source: Bloomberg. Data as of Sep-2020

Source: Bloomberg. Data as of FY2020. OCF – Operating Cash Flow, EBITDA – Earnings before interest, taxes, depreciation & amortisation

All the above discussed factors are ownership neutral, however the prevalence is much more widespread in certain sectors. With the mandate of managing funds, our efforts are to factor in these risks while making investment decisions. In many such cases it’s difficult to quantify such risks creating added uncertainty on what is the ideal multiple, cheap becomes cheaper and finally erodes the ‘Value’ of businesses. When ‘Value’ comes to mean merely cheap valuation multiples and fails to account for the many risks that we have detailed above, the approach tends to have poor outcomes. Our approach to ‘Value’ is guided by ‘Intrinsic value’ and we pay close attention to the many pitfalls that make stocks appear statistically cheap. In the words of Howard Marks, the choice is between value today and value tomorrow.

Product Label

Disclaimer: The chart/s above is for illustrative purposes only and should not be construed as advise. The above is to illustrate the concept of identifying stocks/ sectors in the market and not an endorsement by the Mutual Fund and AMC of their soundness or a recommendation to buy or sell these stocks at any point of time. There is also a possibility of the expected event not happening or some other unforeseen event that may affect performance of the company. The performance of stocks would ultimately depend on various factors such as prevailing market conditions, global political scenario, exchange rate etc. Investors are requested to note that there are various factors (both local and international) that can have impact on the future performance and expectations of any company. There is no assurance or guarantee of any company being able to sustain its performance in future and above information should not be construed as research report or a recommendation to buy or sell any security.