- 4 views

The Reserve Bank of India's (RBI) Monetary Policy Committee (MPC) voted unanimously to hike the repo rate by 50 bps to 4.90%. Consequently, the standing deposit facility (SDF) rate stands adjusted to 4.65% from 4.15% and the marginal standing facility (MSF) rate to 5.15% from 4.65%. The MPC maintained its “withdrawal of accommodation” stance while dropping the phrase “staying accommodative”, signaling a shift towards “neutrality”. The Governor reiterated that further monetary measures will be needed suggesting further rate actions to move towards a positive real rate in near term. The governor also avoided committing on his liquidity stance going forward stating that participants have option of “repo” window in case liquidity becomes negative.

The rate decision was broadly in continuation of “priority shift” since April 2022 policy & was in line with consensus market expectations of frontloaded normalisation of policy rates closer to pre-pandemic levels by August 2022. With the 90bps rate headline hike & an effective rate hike of 130bps since March 2022 (change in overnight rate from 3.35% in March to SDF rate of 4.65%), RBI has joined the group of 15 major central banks who have hiked their policy rates by 50bps & beyond since April 2022 as inflationary pressures ratchet up.

The MPC had highlighted five major risks in its April resolution to the baseline inflation and growth trajectory:

- The ratcheting up of geopolitical tensions;

- Generalised hardening of global commodity prices;

- The likelihood of prolonged supply chain disruptions;

- Dislocations in trade and capital flows; and

- Divergent monetary policy responses and associated volatility

Although it was expected that these risks will play out over time, most of these risks have broadly materialised. While recognizing drivers of inflation as largely exogenous, there seems to be a widespread consensus amongst MPC that persistent elevated inflation can potentially de-anchor inflation expectations & hence it wants to pre-emptively control the spill-over effects and protect the credibility of its price stability mandate.

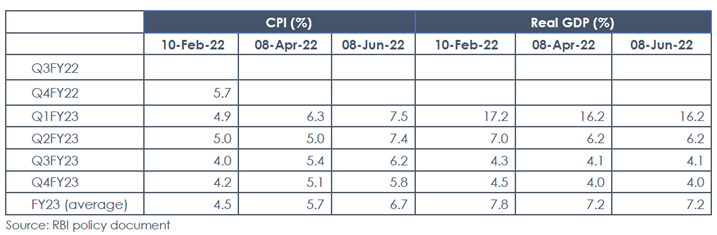

Below are the key RBI’s estimates on evolution of growth/inflation trajectory into the next year compared to their previous forecasts:

As can be seen in the table above, the RBI started this year expecting inflation to slow to 4.5%. As we had noted in our Dec’21 fixed income outlook (https://www.utimf.com/articles/outlook-on-fixed-income-2022), the RBI’s benign view on inflation was predicated on low food inflation, which was at risk given the global stockpiling of food reserves & dry weather. The geo-political tensions in Europe further exacerbated the pressures on an already stressed supply chains forcing the RBI to raise its forecast to 5.7% in March. Even though the MPC hiked repo in May, the panel left the outlook untouched since it was an off-cycle meeting. RBI has further updated its inflation forecasts today considering the elevated commodity prices; revisions in electricity tariffs, high domestic animal feed costs; continuing supply chain bottlenecks & rising pass-through of input costs. Crude prices have been assumed at $105 which could impart upside risks to these estimates. Given that the RBI has not considered any impact on growth of its monetary policy actions, it has also given benefit of doubt to the inflation forecasts.

While the RBI didn’t hike CRR, further actions on liquidity can’t be ruled out given that the RBI took comfort from moderation in headline liquidity which may reverse on government spending/seasonal flows.

Outlook:

The bullwhip effect & normalisation of supply chains eventually leading to manufacturing disinflation: - one of the key expectations of major central banks last year has started to show very initial signs in some of the advanced economies most notably in the US. Concerns have begun to emerge that aggressive policy tightening, geo-political tensions & extremely aggressive Covid control measures by some countries could lead to a prolonged stagflation & possible unwinding of the tightening in 2023-2024 by various central banks. However, as we move from “unprecedented” to “unchartered” territories, it might not be very prudent to form extremely long-term hypothesis as we assess whether central banks remain committed to managing inflation expectations at the cost of growth or let go of their inflation targeting mandates in case of a meaningful growth slowdown.

We believe that the RBI had decisively shifted towards achieving its inflation target of 4% in the April 2022 policy. Given the glide path towards 4% could be unwieldly due to the supply side shocks, it would require MPC to front load its policy actions & maintain a positive real rate for an extended period of time to establish a “sense of credibility”. Given the unusually uncertain environment, the RBI has understandably refrained from committing to a terminal rate for now. Market participants will be keenly looking at the RBI at the upcoming policies to assess direction on terminal rate which we believe could be the next big trigger apart from evolution of inflation.

Our base case is of a terminal repo rate between 6%-6.5% in the next 12-15 months which we believe is largely priced in the short to medium part of the curve (2-5 year) although near term actions such as change in borrowing mix, possible RBI interventions (Operation twists) & global cues could impart intermittent volatility in the near term. The yield curve which had been considerably steep in the last 2 years has largely flattened on expectations of policy normalisation. However, the expected heavy centre/state bond supply could weigh on the long end of the yield curve (10 year & beyond) in the near term.The envisaged terminal rate, however, might not materialize incase of a sharp slowdown of the global economy due to aggressive rate actions by the US Federal Reserve or easing of geo-political tensions in Europe.

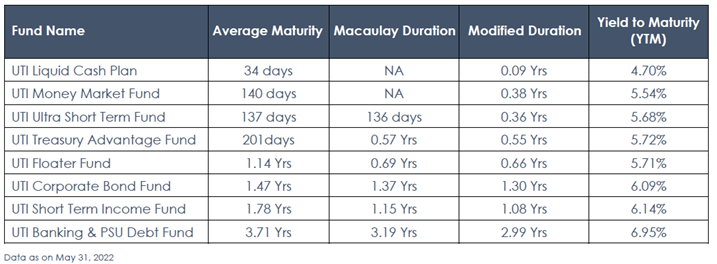

Given the meaningful correction in the last 2 months across the curve, investors with more than 3 year investment horizon can contemplate staggered allocation towards roll down strategies & actively managed duration categories. Investors looking at short term allocations can consider overnight/liquid/money market funds as we navigate near term uncertainty & await RBI’s stance on liquidity/terminal rates in upcoming policies.

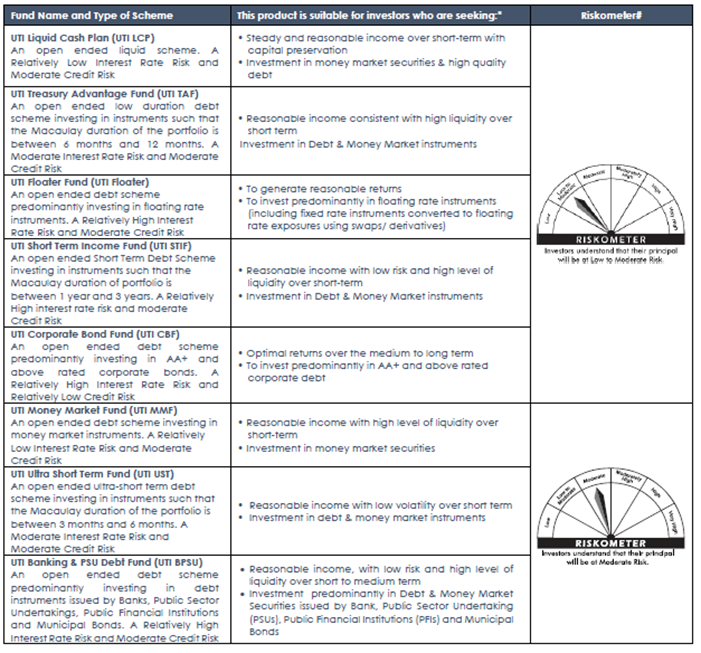

Product Labelling and Riskometer:

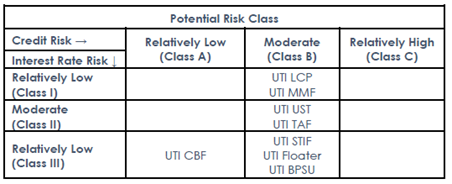

Potential Risk Class Matrix

Mutual Fund Investments are subject to market risks, read all scheme related documents carefully.