Rate action: The monetary policy committee today voted 5-1 to raise the policy repo rate by 35 bps to 6.25%, in line with the market expectations. The external member Prof. Jayant Varma dissented against the decision & voted against the rate hike. The policy corridor floor, the Standing Deposit Facility (SDF) rate, was also hiked by 35 bps to 6.00%, while the ceiling Marginal Standing Facility (MSF) rate was hiked to 6.50%.

Monetary policy stance: More than the rate action, the market participants were keenly watching the policy stance as this policy was expected to offer revealing insights of MPC’s thinking. Views of MPC members had started to diverge significantly on multiple issues like quantum of policy normalization, drivers of monetary policy (currency stability), and terminal policy rates in previous policy itself. Further easing of global financial conditions & views of peak dollar after the better-than-expected outcome in US CPI for November & lack of usual pushback from the Fed Chair during his 30th November speech (Source: https://www.federalreserve.gov/newsevents/speech/powell20221130a.htm) triggered a spate of expectation from RBI to set a tone of final lap of its policy normalization.

However, MPC retained its “withdrawal of accommodation” stance with a 4-2 vote with the 2 external members, Ms. Ashima Goyal & Prof. Jayant Varma, voting against the resolution.

While the stance was in line with expectations, the tone was slightly cautious. Although the MPC expects risks to inflation as “evenly balanced”, both the governor’s statement & MPC resolution cited need to break the persistence of core inflation & lamented upon multiple risks to the disinflationary path such as pending pass through of input costs, high feed costs & continuing geo-political tensions. Governor noted that “Pressure points from high and sticky core inflation and exposure of food inflation to international factors and weather-related events do remain. While being watchful of the impact of our earlier monetary policy actions, we will keep Arjuna’s eye on the evolving inflation dynamics and be ready to act as may be necessary”.

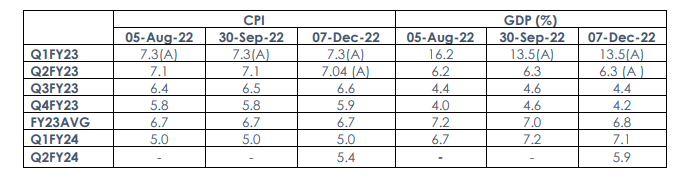

Below are the key RBI’s estimates on the evolution of growth/inflation trajectory into the next year compared to their previous forecasts:

Assessment of inflation:

The RBI retained its FY23 CPI inflation projection at 6.7%, with risks evenly balanced. It projects inflation of 5.0% for Q1 FY24 (April-June) & 5.4% for Q2FY24 (July-Sep). The RBI has continued to assume average crude oil price projection for FY23 at USD100/bbl although lack of complete pass through makes the recent correction less important for inflation although still positive for external account.

Assessment of growth:

The RBI marginally lowered its GDP growth forecast for FY23 (year ending March 2023) to 6.8% from 7% on account of the adverse spillovers from the global slowdown and its negative impact o net exports and overall economic activity. The RBI is optimistic on growth with the prospects of a good Rabi harvest, rebound in services, broad based credit growth, government’ capex & improving consumer confidence & is expecting real GDP growth at 7.1% for Q1FY24 and at 5.9% Q2FY24.

Forward guidance

Interestingly, Dr. Patra alluded to RBI’s Q2FY24 projection of 5.4% as a benchmark for calculation of its real rate of 85bps leaving the scope for a moderate rate hike given RBI’s current preference of a real rate of 80-100bps.

Liquidity

The RBI noted that overall liquidity remains in surplus, with average daily absorption under the liquidity adjustment facility (LAF) at ₹1.4 lakh crore during October-November as compared with ₹2.2 lakh crore in August-September. However, governor cautioned that market participants must “wean away” from the overhang of historic liquidity surplus & RBI is ready to inject liquidity through “LAF operations”, it will look for a “durable sign of turn in the liquidity cycle”. Given the expected natural CRR drain, currency leakage, BoP deficit & periodic tax outflows in the upcoming quarter, we expect short end of the curve to suffer intermittently from frictional volatility as the credit growth & consequently money market (upto 12 months maturity) issuance remains highly robust.

Outlook - Focus to shift to prolonged pause from terminal rates

As we had noted in our April 2022 MPC review, (https://www.utimf.com/articles/rbi-monetary-policy-updates-apr-22/), RBI’s pivot did not just mean pre-pandemic normalisation but anchoring of inflation expectations towards its 4% target. We believed that a terminal rate of at least 6.5% could provide a modicum of sufficient real rate gap. With global central banks still poised for more rate hikes with a preference to err towards caution, MPC rightfully refrained from any strong dovish messaging. However, as we get closer to the terminal policy rate, it’s the expected average policy rate during the projected time horizon which could be more critical in assessing our risk return trade-off than just the peak policy rate. Given that RBI has repeatedly stated their desire towards returning to their 4% inflation target which seems quite far as things stand, we do not expect RBI to follow advanced economy central banks in easing interest rates in case of hard landing concerns as long as India’s growth outlook does not sufficiently deteriorate.

However, one of the positive aspects of this monetary cycle has been RBI’s consistency towards inflation both in terms of action & stance which has largely repriced the curve towards the expected policy rate & we do not expect material disruption from the current valuations although the money market curve could remain volatile in the near term due to the usual quarter ending liquidity & balance sheet pressures.

Given the significant correction on the short end of the yield curve, investors with 6-12 months horizons can consider an allocation to low duration/ money market strategies while investors with more than 3-year investment horizon can consider staggered allocation towards roll-down strategies & actively managed duration categories.

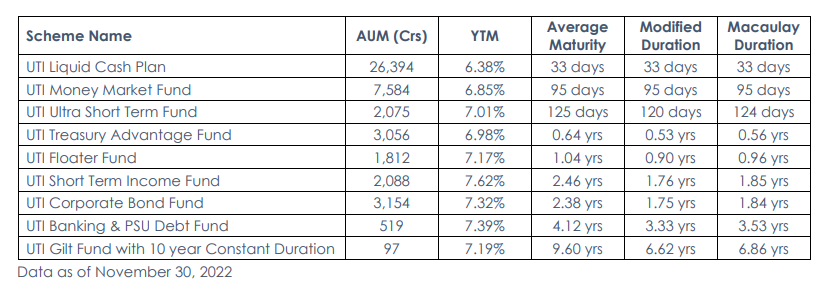

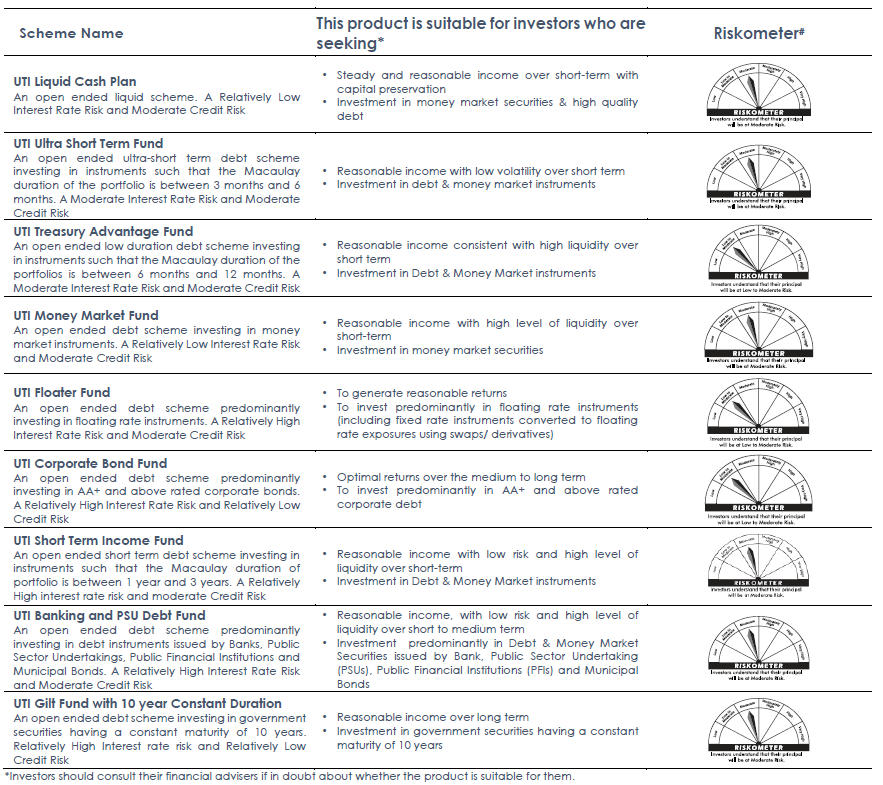

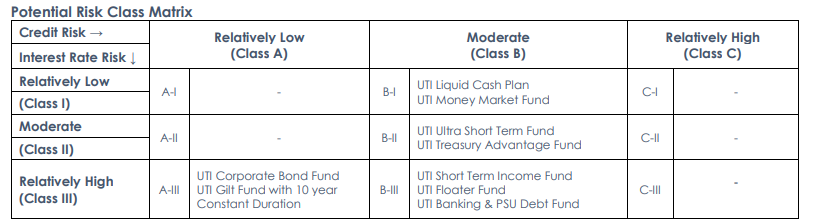

Product Labelling and Riskometer

#Risk-o-meter for the fund is based on the portfolio ending October 31, 2022. The Risk-o-meter of the fund/s is/are evaluated on monthly basis and any changes to Risk-o- meter are disclosed vide addendum on monthly basis, to view the latest addendum on Risk-o-meter, please visit the addenda section on https://www.utimf.com/forms-and- downloads

Mutual Fund Investments are subject to market risks, read all scheme related documents carefully.