- 1 view

Since the last RBI policy meet, global growth-inflation dynamics have changed drastically with increased risks of a synchronized global slowdown due to tight financial conditions & weak consumer sentiment. The US economy registered two consecutive quarters of negative growth. Global commodity prices have fallen meaningfully with Bloomberg commodity & agriculture spot index dropping by 11.3% & 18%, respectively in INR terms since June 8th, the last RBI policy (Source: Bloomberg). Brent in INR terms has also fallen by 19.9% (Source: Bloomberg) while CPI inflation for India during Q1FY23 has averaged 7.3%, lower than the RBI’s forecast of 7.5%.

Compared to many advanced economies, India’s inflation had more of a cost-push element to itself. The bulk of the rise in inflation is driven by higher commodity prices, which were now reversing. According to the RBI Deputy Governor, Dr Michael Patra, two thirds of the change in India’s CPI since the Russia-Ukraine war was reflective of the materializing of geopolitical risk. (Source: RBI, https://bit.ly/3BNkQMy). Moreover, there were few signs of overheating in the Indian economy with India’s GDP marginally above its pre-covid path.

Given the global policy debate on peaking inflation & fears of a mild recession, the incoming expectations from today’s RBI policy was probably a 35-50bps hike but more importantly, a softer policy guidance with acknowledgement from the central bank that the worst inflation was behind us & directional concerns on growth.

The Reserve Bank of India's monetary policy committee today voted unanimously to hike the repo rate by 50 bps to 5.40% while maintaining its stance as “withdrawal of accommodation”. Consequently, the standing deposit facility (SDF) rate stands adjusted to 5.15% from 4.65% and the marginal standing facility (MSF) rate to 5.65% from 5.15%. One MPC member, Prof. Jayanth Varma dissented on the stance.

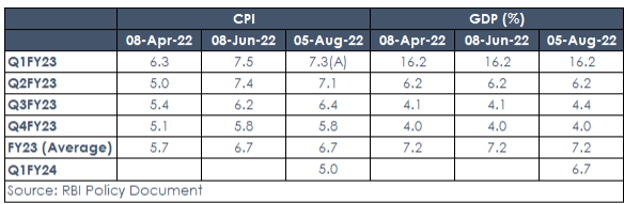

The RBI retained its growth & inflation forecasts provided back in the June policy despite the softening in commodity price, a weakening global growth outlook & impact of tightening financial conditions. RBI seemed to be deriving comfort from the resilient domestic growth drivers with the RBI highlighting increasing capacity utilization, high credit growth & buoyant profitability of the manufacturing sector as well as the impact of imported inflation due to the appreciation of the US dollar.

Below are the key RBI’s estimates on the evolution of growth/inflation trajectory into the next year compared to their previous forecasts:

While the decision to hike the policy rates by 50bps was broadly in line with expectations, the retention of the stance as “withdrawal of accommodation” was seen as disappointing. The sanguine assessment of domestic growth was seen in contrast to global central banks which have increasingly been cognizant of increasing slowdown risks. Moreover, the governor’s statement that the RBI wants to “ensure that inflation moves close to the target of 4.0 per cent over the medium term” was also considered hawkish.

Outlook

During the post policy press conference, on being asked when monetary policy turns neutral, reference was made to the RBI’s monthly bulletin where real neutral rate was estimated at 0.8% to 1% (repo rate minus inflation). Dr Patra also alluded to inflation moving towards 4% target in the medium term as one of the RBI’s milestones. As we had discussed in our June policy communication (https://bit.ly/3Q5exrW), the RBI had decisively shifted towards achieving its inflation target of 4% in the April 2022 policy. Given the unwieldy glide path towards 4%, it would require MPC to front load its policy actions & maintain a positive real rate for an extended period to establish a “sense of credibility”.

We retain our base case of 6-6.5% terminal policy rates given the current growth-inflation trajectory. Any material changes in commodity prices due to a sharp global recession or easing of geo-political tensions in Europe remain risks in our view.

We are in unchartered territories of high interest rates, supply side & geo-political shocks, & hurting consumer confidence. While the worst of cyclical inflation might be behind us, the debate is still open whether inflation will structurally return to its historical trend rates given the global labour market constraints, regulatory shift towards renewable sources of energy, fractured supply chains & stronger household balance sheets.

We continue to be in a period of uncertain forward guidance. This demands higher risk premiums. A data- dependent central bank could also mean more market volatility and surprises in both directions. With the known unknowns on inflation, growth, and liquidity, it will be preferable to wait for better risk premiums on the long end of the yield curve that appropriately value the uncertainty.

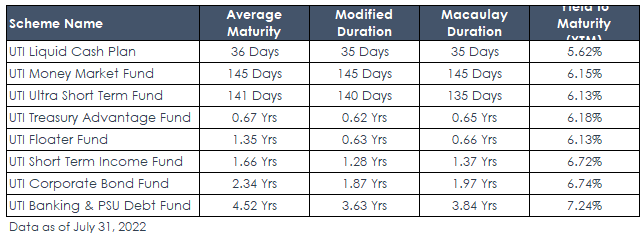

We believe the short to medium part of the curve (2-5 years) has meaningfully corrected & largely pricing in the expected terminal rates although near term actions such as change in government borrowing mix, possible RBI interventions (Operation twists) & currency volatilities could impart intermittent volatility in the near term.

Given the meaningful correction in last 4 months across the curve, investors with more than 3-year investment horizon can consider staggered allocation towards roll down strategies & actively managed duration categories. The money market curve has also reasonably steepened & investors with 6-12 months horizons can consider allocation to low duration/ money market strategies.

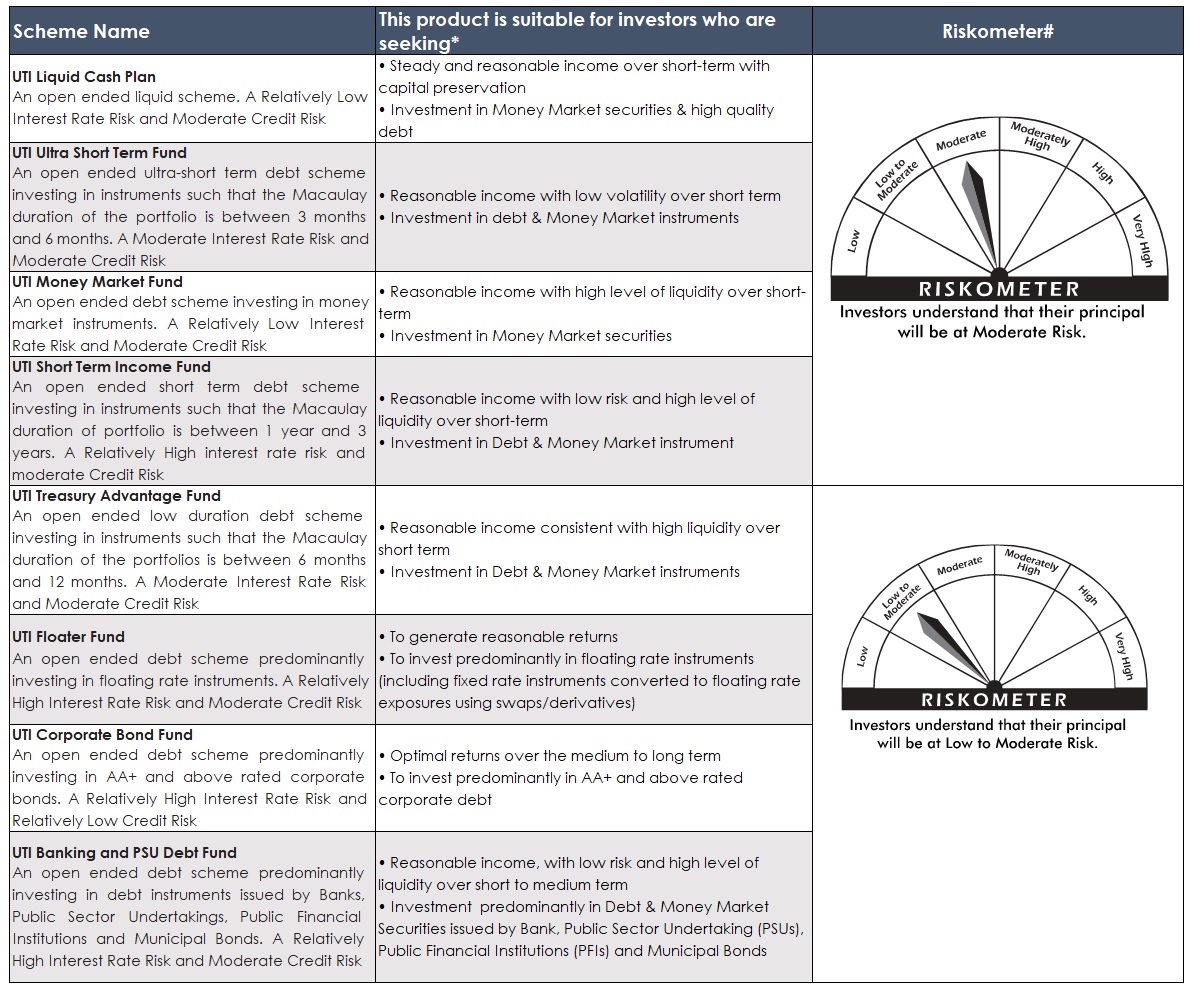

Product Labelling and Riskometer

*Investors should consult their financial advisers if in doubt about whether the product is suitable for them.

#Risk-o-meter for the fund is based on the portfolio ending June 30, 2022. The Risk-o-meter of the fund/s is/are evaluated on monthly basis and any changes to Risk-o-meter are disclosed vide addendum on monthly basis, to view the latest addendum on Risk-o-meter, please visit addenda section on https://www.utimf.com/forms-and-downloads

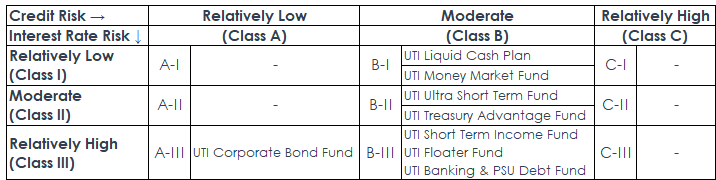

Potential Risk Class Matrix

Mutual Fund Investments are subject to market risks, read all scheme related documents carefully.