The Reserve Bank of India's (RBI) monetary policy committee voted unanimously to keep the repo rate and reverse repo rate unchanged while voting 5-1 to continue with the accommodative stance as long as necessary to revive and sustain growth on a durable basis and continue to mitigate the impact of COVID-19 on the economy.

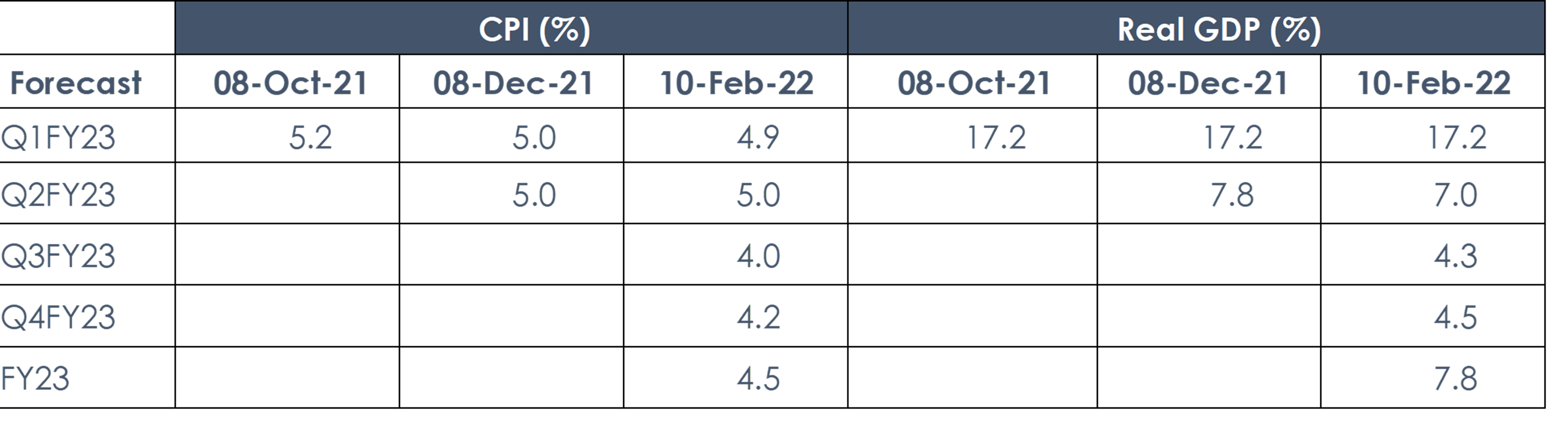

Below are the key RBI’s estimates on evolution of growth/inflation trajectory into the next year compared to their previous forecasts:

Source: RBI policy document

As can be seen from the table above, the RBI has forecasted FY23 GDP growth at 7.8%, lower than the 8-8.5% range as per the Economic Survey for FY23. They have reduced the 2QFY23 growth print to 7.0% from 7.8% in Dec 2021 policy emphasizing weak discretionary demand and adverse global factors. The RBI is projecting FY23 inflation forecast of 4.5%. It expects headline CPI inflation to fall from 5.7% in March 2022 to its 4.0% target by December 2022 due to weak private consumption, decline in price hikes of products & services & fall in vegetable prices.

During the press conference, the Governor clarified about the benign forecast of crude price assumptions wherein he mentioned that RBI will prefer to give it in their semi-annual monetary policy report (to be published in April 2022).

Additionally, certain operational measures on regulation & supervision, liquidity management & market development were announced:

- Restoration of the revised Feb’20 liquidity management framework ( https://www.rbi.org.in/Scripts/BS_PressReleaseDisplay.aspx?prid=49352 ). In view of the pandemic and related work from home and social distancing protocols, the MSF and the fixed rate reverse repo windows were made operational throughout the day, instead of only at end of the day under normal circumstances. As part of its process normalization, the following measures were announced:

- With effect from March 1, 2022, the Fixed Rate Reverse Repo and the Marginal Standing Facility (MSF) operations will be available only during 17.30-23.59 hours on all days and not during 09.00-23.59 hours, as instituted from March 30, 2020

- Variable Rate Repos (VRRs) and Variable Rate Reverse Repos (VRRRs) of 14-day tenor will operate as the main liquidity management tool based on liquidity conditions

- These main operations will be supported by fine-tuning operations to tide over any unanticipated liquidity changes during the reserve maintenance period

- Variable Rate Repo operations of varying tenors will henceforth be conducted as and when warranted by the evolving liquidity and financial conditions within the cash reserve ratio (CRR) maintenance cycle

- Voluntary Retention Scheme limits enhanced to Rs 2.5 lakh crore from Rs 1.5 lakh crore with effect from April 01, 2022. This could provide additional sources of capital for domestic debt markets , including government securities, the RBI said. This route allows foreign portfolio investors easier terms and conditions should they be willing to park their funds for a specified period of time.

- On-tap liquidity facilities for emergency health services and contact intensive service sectors to be extended to June 30, 2022 from March 31 earlier.

- Release of final guidelines for CDS (Credit Default Swaps) to facilitate development of credit derivative market & deepen corporate bond market.

- Permitting Banks to Deal in offshore Foreign Currency Settled Rupee Derivatives Market with nonresidents & other market makers: This could add liquidity to the domestic OIS market & removing segmentation between the onshore & offshore markets.

The backdrop for the February 2022 MPC meeting was probably more complicated than the usual. Since its December policy when RBI chose to keep the reverse repo unchanged as It wasn’t certain whether the economy could tolerate the output sacrifice amidst a backdrop of renewed outbreaks of new Covid variants, growth/inflation dynamics had somewhat evolved.

The impact of new Covid variants on economic activity appears to have been muted. Commodity prices, especially oil has moved up materially. Advanced economies central bank notably the Fed, ECB & BOE had been more emphatic about upside risks to inflation. Overnight rates have been highly volatile due to fine tuning operations, probably not, what the central bank envisaged. Moreover, the growth oriented fiscal path undertaken by the Government in its recent budget exercise probably meant a start towards normalisation for an inflation targeting central bank like RBI.

Majority of the market participants believed that RBI could start with a calibrated hike to reverse repo from this policy.

However, the biggest reason MPC saw not to act perhaps was its outlook on CPI, which it expects to moderate in H1:2022-23 and move closer to its 4% target rate thereafter. The RBI is expecting easing of vegetables prices on fresh winter crop arrivals, softening in pulses and edible oil prices in response to strong supply-side interventions by the Government. Given MPC’s expectation of weak private consumption, it is also expecting subdued pass through of input prices resulting in decline in the pace of price hikes by the manufacturing and services firms going forward. Hence, the bar for future rate action would probably depend on RBI’s outlook on H2FY23 CPI going ahead.

Outlook:

The biggest concern amongst the market participants today was not RBI rate action but its commitment to the smooth execution of the record high Government borrowing program. The Governor reiterated RBI’s strong track record in managing previous 2 years high borrowing & also expressed his intent to carry out the FY23 borrowing program without significant disruptions once the new borrowing program starts although no details were given at this point.

The money market curve (up to 12 months maturity) was already 30-40 bps higher in January after announcement of fine- tuning liquidity operations increased the volatility of overnight rates. Hence, we don’t foresee any meaningful impact of the pause on the reverse repo rate on the very short end of the curve (upto 6 months maturity) although beyond 6 months segment may see some rally due to push forward of rate hike expectations.

Market participants were broadly expecting a 15-20 bps hike in reverse repo hike today followed by full normalisation to a 25 bps corridor & a stance change in April-June 2022 quarter.

However, normalisation expectations could get pushed forward with reiteration by the RBI Governor in his policy statements as well as press conference that their future policy actions will be “calibrated & well telegraphed”. Given that there was no indication of normalisation in today’s policy, barring a meaningful pick-up in economic activity or build-up of generalised price pressures, market participants may not expect aggressive rate action from the RBI at least in 1HFY2023 & the yield curve could remain steep for some time at least till the bond supply picks up meaningfully or the RBI starts rate normalisation.

While investors with a minimum 3 month horizon can consider allocation to Ultra to Low duration categories (including money market funds), given the steep yield curve & RBI’s comfort with current growth/inflation dynamics & patience in policy normalisation, investors with more than 12 months horizon can consider allocation towards Short term & Corporate bond fund categories.

Data as on January 31, 2022

*Investors should consult their financial advisers if in doubt about whether the product is suitable for them.

#Risk-o-meter for the fund is based on the portfolio ending January 31, 2022. The Risk-o-meter of the fund/s is/are evaluated on monthly basis and any changes to Risk-o- meter are disclosed vide addendum on monthly basis, to view the latest addendum on Risk-o-meter, please visit addenda section on https://utimf.com/forms-and-downloads/

Mutual Fund Investments are subject to market risks, read all scheme related documents carefully.