In the Ramayana; Kumbhakarna is described as having been cursed to sleep for 6 months at a time. If only we investors had the same ability. If we had fallen asleep at the end of February 2020 and then woken up at the end of August 2020, it would appear that nothing much had happened. After all the Nifty 50 closed at 11201 at the end of February 2020 and at the end of August 2020 it was only marginally changed at 11387. Just another boring year, would likely have been your reaction if the first thing you looked at was the Nifty 50 value. Then as you read the news you would know about the tragic loss of life and suffering the world had endured due to the first global pandemic since 1918.

You would have missed the roller coaster ride of markets and sentiment through the past six to eight months. In July 2020, in this very magazine we wrote – ‘The virus is not behind us yet but with the world’s best and brightest trying to find cures and vaccines we are hopeful that human ingenuity will see us through this crisis’. That is now a reality with several vaccines receiving approval or in the final stages of receiving approval across the globe. It is now merely a question of when.

Governments and central banks across the globe stepped in to provide financial stability to the markets by providing unprecedented levels of fiscal and monetary stimulus along with other measures to support their battered economies. With liquidity flooding the global markets and major economies showing early signs of recovery, capital has started flowing towards riskier assets including equity markets of emerging economies. With government and central banks showing no signs of letting up on “do whatever it takes” attitude to shore up growth, there is hope for continued strong capital flows into emerging markets.

In India, several metrics now point to sections of the economy having recovered to their pre-pandemic levels of activity. GST collection which provides the fastest and broadest indication of goods production and movement in the economy has moved into positive territory on a year on year (y-o-y) basis. Without a doubt, the recovery is uneven - the formal and organized sector has bounced back quickly, perhaps gaining from larger troubles impacting the informal and unorganized sector. Service sectors such as travel, tourism, entertainment, etc. with a large urban footprint remain disrupted while the agricultural sector has powered the rural economy back to positive growth trajectory.

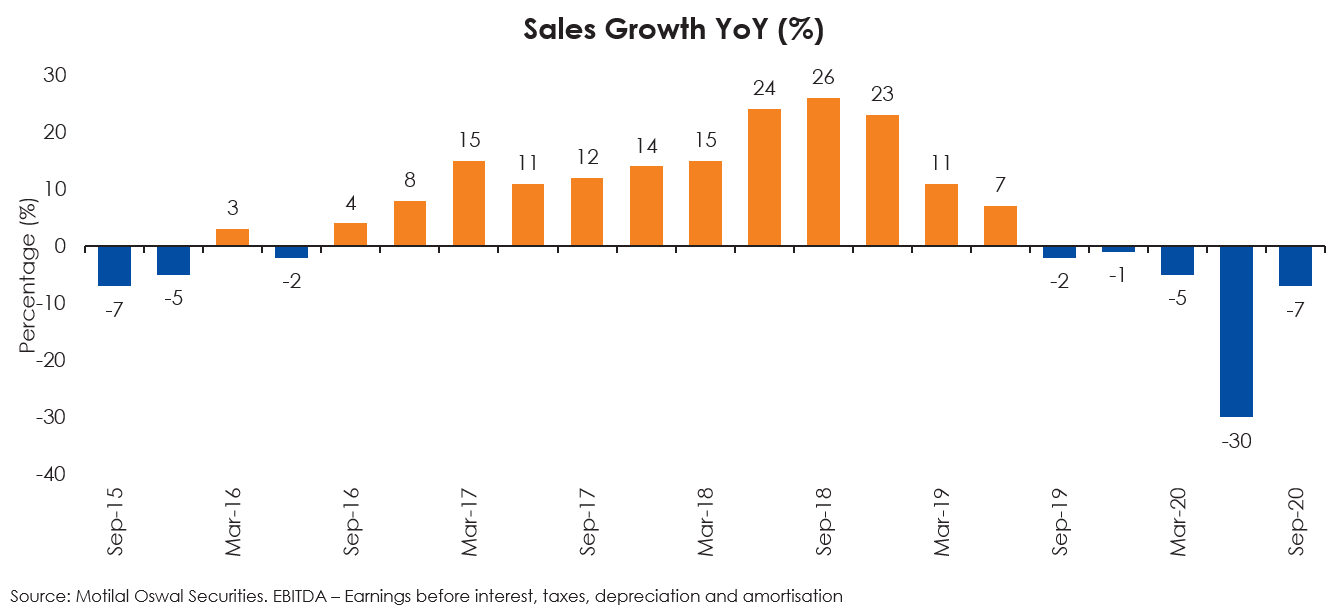

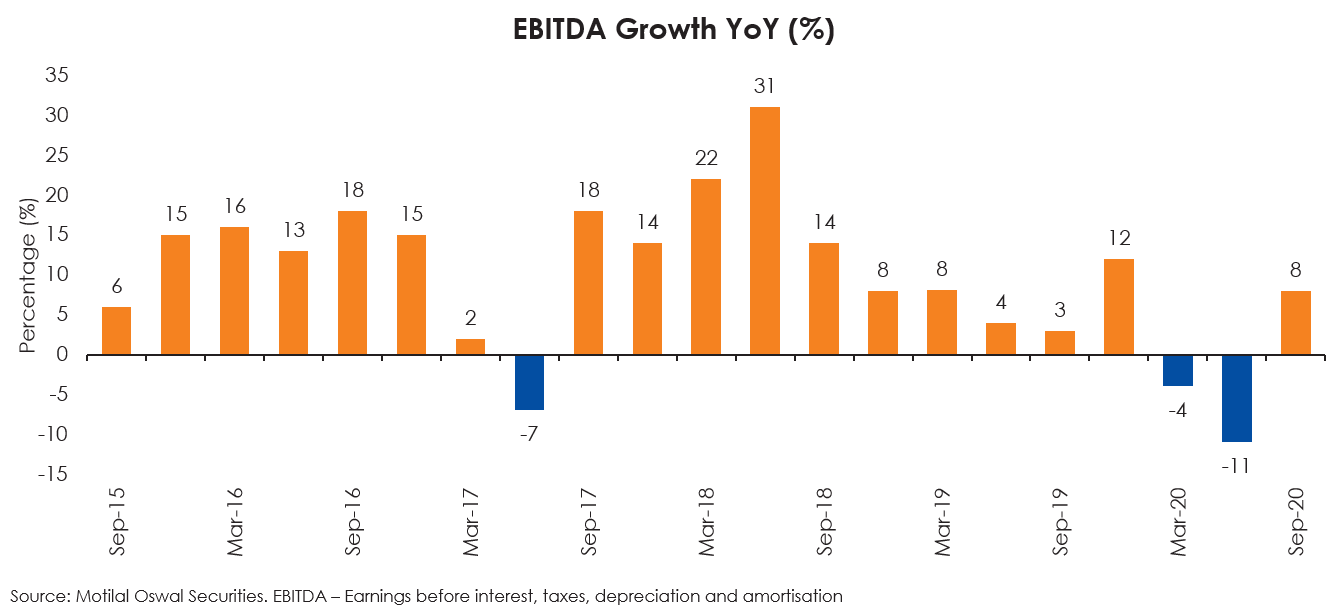

The earnings for the quarter ended September 2020 when the recovery gained steam surprised against all expectations. While revenues for the Nifty 50 companies declined 7% y-o-y in the September quarter; their operating profits (EBITDA) increased by 8% y-o-y. The EBITDA margin for the Nifty 50 (excluding financials) has increased by over 3% from 16.3% in the quarter ended March 2020 to the 19.8% in the quarter ended September 2020. The margin expansion reflects both reduced competition and cost savings. It is likely that this is not entirely sustainable in the long term but for now it is further strengthening corporate balance sheets.

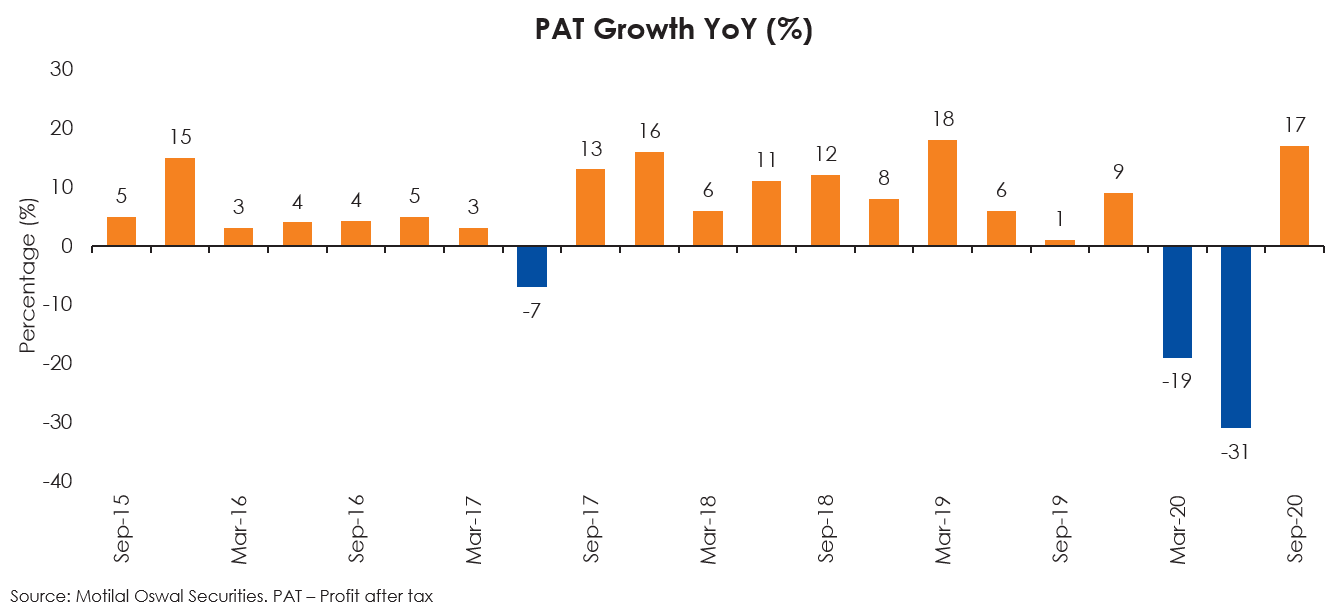

There has also been a significant drop in interest rates, and this is transmitting into the income statements of companies. As a result, the Profit after tax (PAT) of the Nifty 50 companies grew by 17% y-o-y vs an expected decline.

In July 2020, we also wrote - …the baton now passes from valuations to visibility of growth and earnings. The results of the quarter and the continued buoyancy in economic indicators in the current quarter bode well for earnings in the near-term. The bar is set high as the Nifty 50 Bloomberg consensus now forecasts 38% growth in FY22 earnings after a flat forecast for FY21 earnings.

In addition to a supportive fiscal and monetary policy outlook in India, we also have the potential benefit that could accrue from several supply side reforms undertaken by the government during this year. These reforms relate to the agriculture sector and the labor codes. The Production Linked Incentive (PLI) program rolled-out by the Government of India (GoI) bolsters the case for a pick-up in the investment cycle in India. The significant fiscal benefits being offered via the PLI scheme along with the lower tax rates announced for companies in 2019 raises the attractiveness for new investments despite the moderate levels of capacity utilization. The targeting of the PLI, to attract new investments where India has a manufacturing shortfall or to participate in global supply chains bypasses the capacity utilization issue in part.

Valuations are no longer as attractive as they were at the trough in the middle of this year, but the prospects are bright. It would be best for investors to stick to their asset allocation targets and invest in a staggered manner. It is always the case that cheap valuations are accompanied by bad news and uncertainty about the future, just as expensive valuations are accompanied by good news and confidence about the future. The Kumbhakarna approach of sleeping through volatility & news flow by sticking to a predefined investment plan has much merit.

| Above article was written for and published in HDFC Bank's AAG Magazine, December 2020 issue; a monthly magazine published by HDFC Bank which is circulated among their HNI clients. |

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY