- 3 views

We have often heard this phrase in relation to sports, especially when top-notch players seem to be going through a rough patch. Many of us may recall how the same was said about former cricketer Sachin Tendulkar when he was going through a similar phase. It was only after he scored his 100 th century that his critics accepted that ‘class is permanent’.

Today, when people question cricketer and former captain Virat Kohli's form across the formats, his ardent supporters rightly quote this adage to justify his presence in the Indian team. The quote, which possibly goes back to the legendary Liverpool football manager Bill Shankly, has found resonance in the investing world as well.

If one were to draw an analogy between high-quality companies as one that has "Class" looking at the past track record of companies there is high persistence to remain a high-quality or high "Class" company in the foreseeable future.

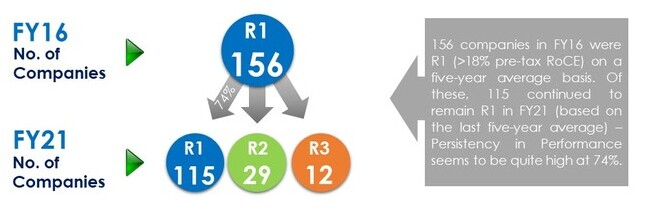

High persistency: 74% of R1 companies in FY16 remained R1 in FY21

ScoreAlpha: UTI Equity Investment Process — As a part of the investment process, companies are rated based on their Return on Capital Employed (RoCE) / Implied Return on Equity (RoE). The 3-tier rating process called R1/ R2/ R3 is based on the previous five-year average return on capital (for manufacturing companies and non-lending non-banking finance companies (non-lending NBFCs). The rating is based on the previous five-year average return on asset for banks and NBFCs (including housing finance companies).

From the above empirical analysis, we can establish that “class is permanent / persistent”.

It is possible, though, that some companies or their moats may face challenges from time to time. It may so happen that some aspects of their quality come under question or that the sector goes through a period of macro difficulties that may hit even a high-quality company. As per our observation over the long-term, such high-quality businesses tend to come back stronger from downturns. These companies, also called ‘Large-cap Isotopes’, have high quality (RoCEs in the R1 bucket), leadership, balance sheet and management quality like a large-cap, but they operate in a niche sector where large-caps have less representation. Read more on Large-cap Isotopes.

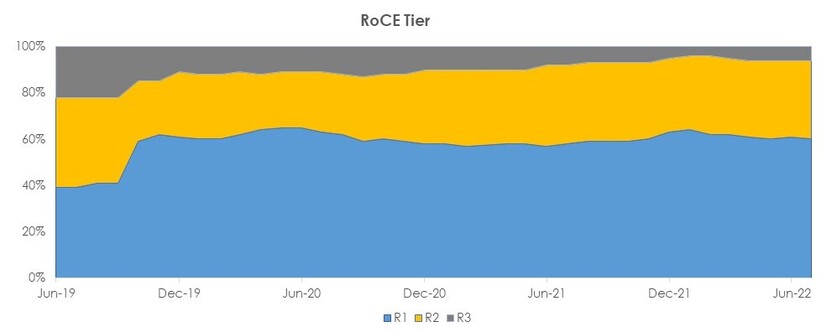

We have also observed that some of these companies experienced a drop in last year’s RoCEs, as it was a challenging phase with commodities surging high coupled with various other disruptions. Hence, for a year, some companies saw a lower RoCE profile than the index. However, our understanding says that as these companies emerge from a trough year, their RoCEs shall significantly improve as the long-term average RoCE remains relatively high.

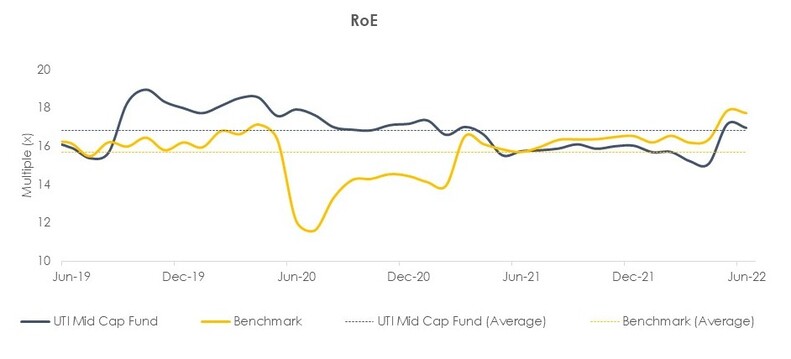

For more details, please refer to UTI Mid Cap Fund Presentation (July-2022)

As R1 companies have pre-tax RoCE of 18% on an average over the preceeding five years period. A company in the R1 bucket is typically high-quality and it remains stable over time. One bad year may not significantly shift the R1, which is a stable metric to track the performance of companies. Therefore, R1 company would be an indicator of “Class”.

Trend in aggregate Return on Equity (RoE)

For more details, please refer to UTI Mid Cap Fund Presentation (July-2022)

Many companies in consumer discretionary have had a tough year owing to weak macro with respect to last year’s multiple headwinds. Some companies currently may be going through a loss of form in the near-term due to bad macro. FY21 was also impacted by the pandemic, which hurt some segments of the markets/ economy much more than others, and depressing RoCEs on an aggregate basis.

But our sense is that much like Virat Kohli and Sachin Tendulkar, these companies are going through a rough patch. And, once they come out of this trying phase, their permanent class would also help improve overall and near-term RoCEs.

Our advice to investors is to look at long-term form of companies and use that as an anchor of performance, because ‘form is temporary, but class is permanent’.

Product Label:

| UTI Mid Cap Fund

An open-ended equity scheme predominantly investing in mid cap stocks This product is suitable for investors who are seeking*:

*Investors should consult their financial advisers if in doubt about whether the product is suitable for them. Risk-o-meter for the fund is based on the portfolio ending July 31, 2022. The Risk-o-meter of the fund/s is/are evaluated on monthly basis and any changes to Risk-o-meter are disclosed vide addendum on monthly basis, to view the latest addendum on Risk-o-meter, please visit addenda section on https://www.utimf.com/forms-and-downloads/ |

|

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.