- 2 views

I am not a cook, but watching people cook, especially in a contest, is surprisingly captivating. Have you ever wondered that in a multitude of these Masterchef type contests, there would be a set of amateur chefs who would be given the same type of "wonderful" ingredients, but each would make a significantly different dish out of them, which would then lead to either win or lose in their pursuit of being the best Masterchef.

Promoters of companies are like Masterchefs who have been given a similar set of ingredients like people, capital, infrastructure, rules and regulations etc., but what they make of it, the dish (or the company) is entirely different. A significant part of investing in businesses, especially ones in the early stage of their growth cycle, is our ability to judge a promoter (or the Masterchef) on various parameters like integrity, capability to run a business, and long-term promoter's vision.

First principle of investing - avoid investment indigestion

I would say that integrity of Promoters is a critical aspect of "exclusion" when we are looking at businesses. Poor integrity promoters are like those restaurants that don't take care of the products and hygiene of their processes to cook and can give you indigestion. So that your investments don't get indigestion, it is crucial that you immediately weed out companies that are run by promoters that could have integrity issues.

There are umpteen examples of companies that have caused wealth destruction in the past where companies have been caught fudging accounts, overstating numbers or diverting capital.

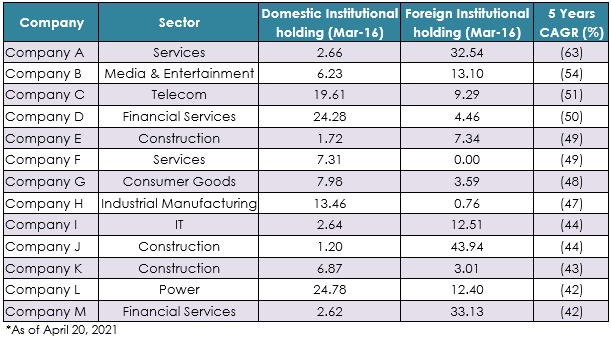

Many investors would have lost much money investing in companies that were much liked at one point. Then they get disappointed over a period of time. If one analyses these companies, then there would be a similar thread of poor governance, misallocation of capital, poor management running across many companies (possibly not all and some may even be impacted by exogenous factors). Below are the companies (without names) that have destroyed investors' wealth in the last five years. Many of these were owned by a lot of institutional holders. Avoiding these businesses is one of the most challenging tasks for any investment manager.

So, the question now arises is that, how should one know if the promoter has integrity issues -

Analyse cash flows -

"P&L is vanity and cash flow is sanity" - Any promoter can fudge P&L to overstate earnings but operating cash flow is reality and cash on the balance sheet - verifiable if investment in liquid MFs or bank accounts (maybe one should be wary of cash tucked in some foreign entity and never repatriated).

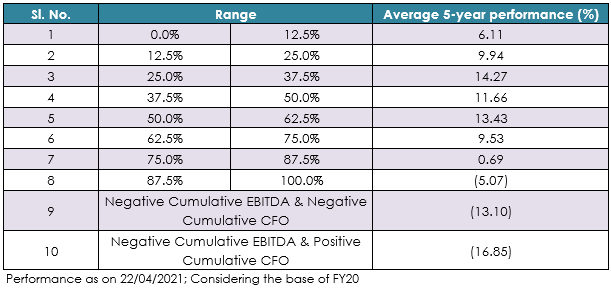

Below table takes the S&P BSE 500 index and its constituents 5 years back and divides the constituents into 8+2 groups based on the EBITDA to CFO ratio. So the 0-12.5% are the top 1/8th of companies on EBITDA to CFO conversion.

In the above table, it is clearly visible that as the EBITDA to CFO conversion starts deteriorating the performance of companies also deteriorates. In fact, companies with cumulative 5-year OCF is negative the average performance is quite poor.

Within our investment framework also we divide companies into 3 buckets C1, C2 and C3 - across periods we see that the performance of the C3 buckets which has the most volatile cash flows is the worst.

Other areas to look for red flags

- Look for the related party transactions and unlisted entities - if a company is doing much business with related entities and many of them are unlisted, it could be that the firm is accounting for costs elsewhere.

- Do common-size P&L with other companies in the sector - if a sharp divergence exists between the companies that is being analysed versus the other players in the industry, it should be questioned.

- Some other tools like fraud detection tools (Beinish m-score) could also help look for red flags for the companies.

- Promoter salaries, CFO salaries / board composition, attrition in the board, outside interest of promoters, past track record of governance, any defaults in the past on payments especially to financial companies etc can be other areas to look at for red flags.

Case Studies

Case Study 1: Jewelry business peers comparison –

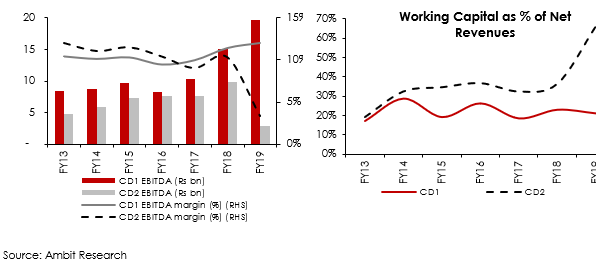

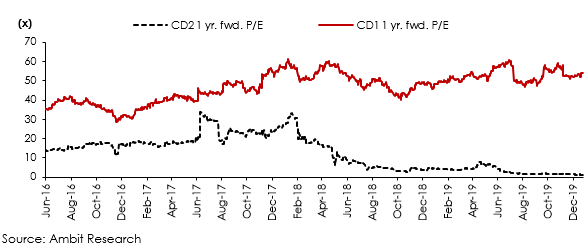

Comparison with company that has a proven track record of governance can also give some insights into the quality of reported earnings for mid and small cap peers. In the below example CD1, CD2 are two companies in the listed space – one of them has a much better track record of governance.

| CD2’s EBITDA margin, once equivalent to CD1, was reduced to just 3% in FY19 | In FY19, working capital as % of revenue for CD2 jumped to 66%! In contrast, over FY15-19, we didn’t observe material change in working capital intensity for CD1 |

Once there was a sharp divergence in operating performance and working capital management of the company, a sharp derating in the stock followed.

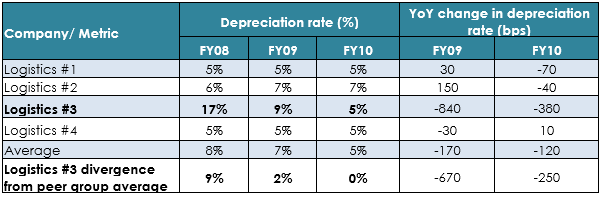

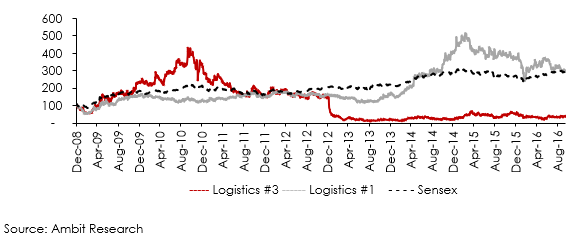

Case Study 2: Logistic company –

Showed a significant change in depreciation rate – a metric that should largely remain stable.

What followed after a while was again a sharp derating in the company.

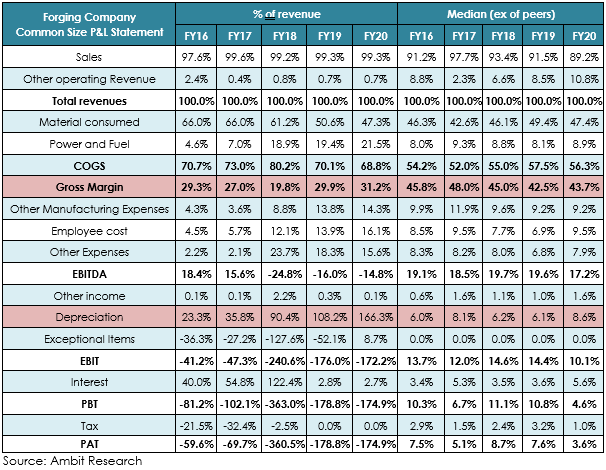

Case Study 3: A forging company

The forging company had significant differences from some of its listed peers when looking at various operating metrics. The company was seemingly overstating its gross block, also reflected in significantly lower (almost half) the asset turnover of the other listed peers. The shares of the company are no longer traded and suspended.

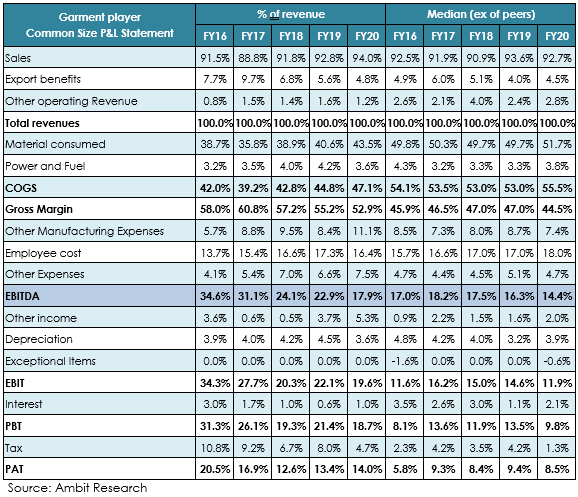

Case Study 4: A garment manufacturer –

This south based garment manufacturer on the face of it looks good as the margin profile is relatively superior to others in the industry. However, if one were to look at the related party transactions, then one would figure that lot of the costs were possibly being reported in an unlisted entity which was causing the margins to look better than other listed peers.

Story of the company in the last five years

CFO salaries – Generally, if you have a CFO who is getting paid much less is primarily someone who is not senior enough in the industry to see any reputation risk from being associated with a company with poor governance. One should be wary of companies that are paying too little to the CFO function.

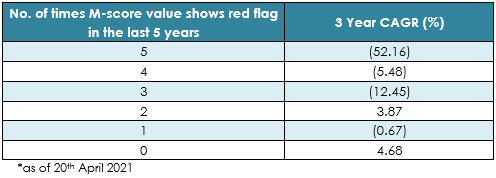

Beinish M-Score – We analysed companies that showed a red flag in the last 5 years and grouped them to see the average performance of companies in the previous 3 year period for these companies. We have seen that companies that have higher red flags on average tended to perform poorer over the last 3 year period than those with lower red flags.

Channel checks

Channel checks are an important way by which one actually can do a qualitative assessment of the company. Typically, a promoter with integrity issues in one aspect would also not be fair to his employees. He may have problems with his distributors, vendors, clients, too flamboyant or gives aggressive guidance or uses shareholder money for self-aggrandizing opportunities. Hence, taking feedback from peers, ex-employees and doing channel checks on the company is an essential way by which one can ascertain not just the integrity aspects of the company but also how it is positioned within the peer group.

- Microfinance companies – There are many microfinance companies in the unlisted space that can give you fair feedback about the practices of many microfinance companies on the ground. For example, it was a well-known fact a few years back that one of the largest microfinance company based out of Karnataka had aggressively given loans to its customers and then it later came to haunt them as large NPAs during periods of crisis.

Capital allocation

Like for any Masterchef, the combination of ingredients one chooses is critical; some elements go well with each other while some won't. Likewise, promoters need to be wise about their capital allocation. Often, promoters spend their energies in acquisitions and ventures that are not in alignment with their core business; this could lead to significant wealth destruction in companies. Promoters are judged over time how they are allocating precious capital and that they are not investing it in negative NPV projects.

- A large media broadcaster - Misallocation issues - There is a case of possible misallocation of capital or over investment in content inventory that is difficult to account for as the probable return on that investment could be back ended.

- A leading auto company focused on multiple businesses (Company X) - course correction on investments - Company X is trying to course correct from a slew of investments where they forayed into many international geographies. Unfortunately, most of the investments there turned out to be value destructive. The group is now on a course correction to create value for its shareholders, which re-emphasizes how important capital allocation is for value creation in any business. The value creation path involves exiting from businesses with no path to profitability and only retaining ones that can create value for shareholders.

- Promoter of an erstwhile alcoholic beverage company - Once present in a profitable business, the entry into Airlines proved to be the undoing of the company and most importantly the promoter.

- Leading diesel genset player - NBFC business was quite lucrative at one point in time and saw the entry of non-related participants. Before the ILFS crisis, everyone was queuing up to get an NBFC license. That is why initially when the company, talked about investing Rs.1,000 crore in a NBFC business where they had no business to be at least under the listed entity then that certainly raises a red flag. The market has duly derated the stock in the last couple of years.

- One of the leading staffing companies moved away from its core business and began investing in unrelated or vaguely related business. Further, the company made an investment in a sports club. Certain accounting practices adopted by the company were also seen as aggressive. The capital allocation decisions resulted in a severe de-rating of the company. The company used to trade at a premium to its peer, but it started trading at a discount due to the capital allocation decisions. The company is now on a course correction, and they have taken measures to rectify and write off some of these investments.

In summary, any business that one invests in, especially at an early stage of the growth cycle one needs to also back the promoter who is running the business and what sort of succession plan the company has, whether there are processes set for the longevity of the firm, any conflict within the promoter group because these soft factors can either re-rate or derate a business. Promoter is a key steward who can take the company to new heights. Everyone makes mistakes and not to say that Promoters of companies cannot, and many times when they recognize these mistakes and take steps to correct them, the market also takes it positively. So there is redemption as long as the promoter understands the fact. At the end of the day few bad dishes should not be the end of the journey for any professional chef.

So remember, next time (and whenever that happens) you go to a restaurant, maybe you will have a greater appreciation of the chef who cooks that delectable plate of food for you - cause he (promoter) could really make or break your experience (investment in a company). For the time being just enjoy their genius from the comfort of your house.

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.