UTI Value Opportunities Fund is an open-ended equity scheme that follows a value investment strategy. The Fund follows the principle of intrinsic value — instead of the traditional multiple-based definition of value for portfolio management. Intrinsic value is ‘the discounted value of cash generated by a business during its remaining life’. The Fund has a flexible approach in terms of investing across the market cap spectrum based on available opportunities.

For an investment strategy to be successful, the strategy followed cannot be static. Instead, it must evolve through changing market dynamics. However, it should not be so malleable either that it does not have any core levers. In the case of UTI Value Opportunities Fund, we have three key tenets, which are used to navigate the portfolio while retaining its core philosophy.

Key Tenets of the Investment Strategy

Valuation Filter for Sectoral Allocations

This is the first lever that is used to apply valuation filters for sectoral allocations. The decision is largely driven by valuation consideration. In the case of cyclical sectors, asset based-metrics or book value-based metrics work as better guides when it comes to judging the sector in terms of history as far as valuation is concerned. Earning metrics can be misleading in cyclical sectors during market turns.

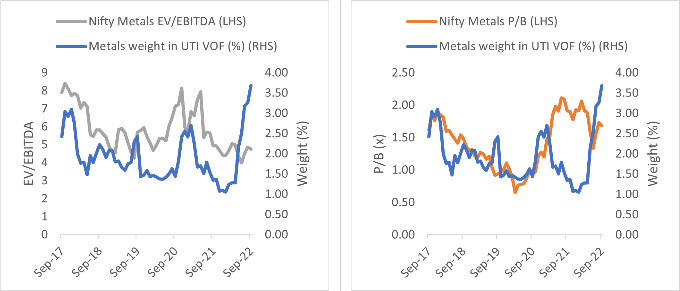

For metals, we prefer the Price/Book metrics to move allocations of sectoral weights, as EV/EBITDA was cheaper during cycle peaks and expensive during cycle troughs.

Valuation of Metal Sector v/s Fund's Exposure

Earning-based metrics that assess valuation comfort or froth are useful for stable sectors or less cyclical sectors.

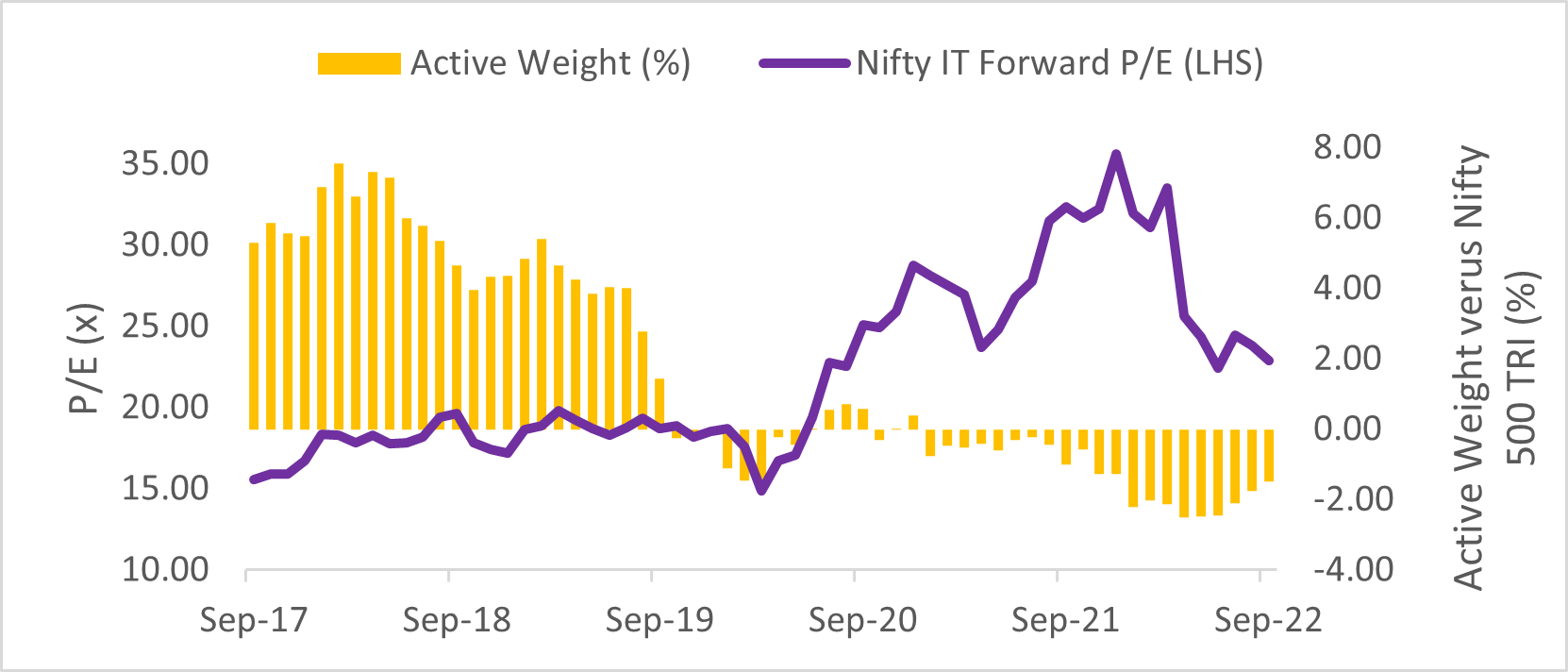

The IT sector was going through a tough phase in 2018 since growth was subpar. However, the valuation was cheaper in comparison to the market as well as history, based on traditional metrics like FCF yields or PE. This trend reversed in late 2021, with the entire sector being rerated on the back of significant growth. The implied growth as reflected in valuation, moved from single digit in 2018 to mid-to-high teens in late 2021.

We followed our core approach to reflect our views on valuation in sector allocation in both cases.

Valuation of IT Sector v/s Fund's Exposure

We follow a similar approach for allocation in the healthcare sector, which has seen significant derating since CY 2015/16. However, the risk of generic price erosion and FDA inspection related events seem to have capped valuation in this sector.

In terms of sector allocation, we choose to participate in situations of sector level mispricing, which generally do not sustain. We also prefer to participate in sectors that have seen supply cuts or disruptions, with demand largely remaining intact.

Barbell Approach for Stock Selection

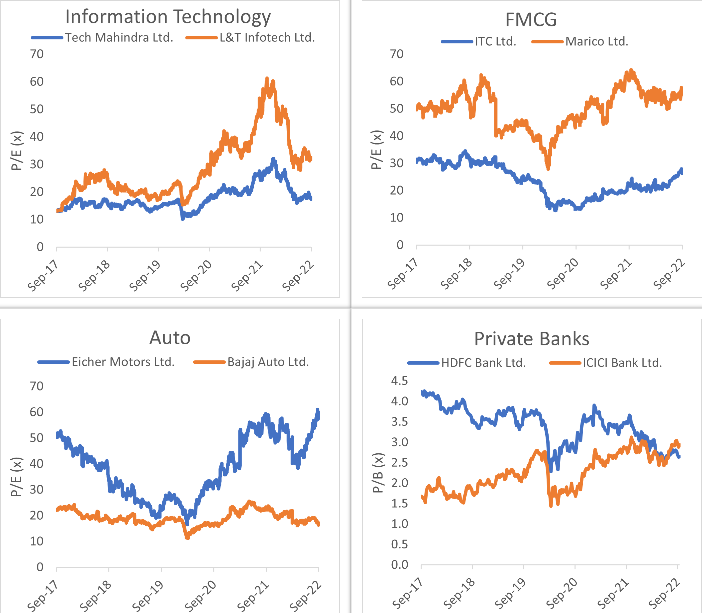

This is the second lever that is used for stock selection. Here we use the analogy of a barbell, an exercise equipment, which has weights attached at both ends of the bar. In UTI Value Opportunities Fund, we apply this concept by investing in two different sets of companies to achieve that same sense of balance.

On the one hand we invest in firms that are going through cyclical downturns and have limited terminal value risks, while the market is excessively focussed on current downturn ignoring the potential turnaround/ cyclical nature of business. On the other hand, we focus on stocks that have high growth potential, have long runway for growth and strong franchise, which are often underappreciated. In both these cases, we are buying something cheaper, relative to expectations, while taking exposure in cyclical as well as growth- oriented stocks, essentially with weights at both ends of the barbell.

Our philosophy in portfolio construction for the fund is to avoid taking balance sheet risk while buying value stocks, though P&L risks are unavoidable. We also avoid stocks that have implied growth built-in prices, which is either unsustainable or significantly higher than delivered growth over the last decade.

Examples of Barbell Approach in Stock Picking

Flexibility to Move Across Market Cap

This is the third lever that is used in a more measured manner. This is used to move portfolio allocation based on valuation differential in large, mid, and small cap. Our range of allocation outcomes to mid and small cap have broadly ranged between 18% to 35% over the last five years. We believe such allocation changes work more in small cap rather than mid cap that demonstrated relatively stable outcomes.

Our Portfolio Allocation Approach

Using these three core levers we end up with portfolio level valuation, which are cheaper than our benchmark on aggregate basis, reflecting the value orientation of the fund. Price/Book Value (P/B) is used as preferred metrics to judge our positioning with respect to benchmark, as far as valuation is concerned. We use P/B as it is less volatile and because higher allocation to cyclically challenged companies do not distort this metrics, unlike earning-based valuation metrics such as Price/Earnings (P/E) or EV/EBITDA.

Adhering to our conviction-driven approach to investing, we generally do not have any non- zero underweight exposure to stocks. We either have an overweight position with respect to the benchmark in a company or we have zero allocation to the company. This is reflected in high active share of 60-70% in the portfolio, which has been consistent for the last few years.

We believe that the use of valuation as a tool for sector allocation — while investing at both ends of the barbell at a stock level helps in consistent return outcomes, as compared to having a fully cyclical orientation in our portfolio, which often leads to volatile return outcomes for investors.

To read the more on “What is Value Investing?” click here Part 1 and Part 2

Product Label:

| UTI Value Opportunities Fund

An open-ended equity scheme following a value investment strategy This product is suitable for investors who are seeking*:

*Investors should consult their financial advisers if in doubt about whether the product is suitable for them. Risk-o-meter for the fund is based on the portfolio ending October 31, 2022. The Risk-o-meter of the fund/s is/are evaluated on monthly basis and any changes to Risk-o-meter are disclosed vide addendum on monthly basis, to view the latest addendum on Risk-o-meter, please visit addenda section on https://www.utimf.com/forms-and-downloads/ |

|

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.